Electric mobility is scaling faster than wired infrastructure was designed to handle. Wireless charging is no longer a convenience feature, it is becoming the architectural backbone of autonomous, electrified transport.

The International Energy Agency confirmed that global EV sales reached nearly 14 million units in 2023, representing 18% of all cars sold up from just 2% in 2018. That exponential curve is already stressing conventional charging infrastructure in dense urban and fleet contexts. The response is not simply more cables. It is a rethinking of how energy integrates with mobility, and intellectual property is now where that rethinking is most intensely contested. As governments and automakers accelerate electrification, wireless EV charging is emerging as a scalable alternative to conventional EV charging infrastructure, reducing dependence on physical connectors while improving user convenience.

Three Inflection Points Reshaping the Technology

Wireless EV charging is not a single technology. It is a convergent stack of coil topology, magnetic shielding, silicon carbide power electronics, alignment algorithms, foreign object detection, grid interface controls, and communication layers. Each layer is IP-protected or contested. And today, three structural shifts are simultaneously redefining what the technology is capable of.

Beyond Passenger Vehicles

Systems are scaling from 11 kW passenger applications into 200–750 kW freight and heavy-duty platforms, introducing new thermal constraints and high-power converter architectures.

The evolution of wireless charging platforms for buses, logistics fleets, and commercial vehicles demonstrates that the technology is expanding far beyond private mobility use cases.

Charging While in Motion

In-road charging moves innovation from vehicle hardware to civil infrastructure, expanding the patent battlefield to include roadway integration, segmentation logic, durability engineering, and grid coordination. Europe leads pilot programmes; scalability at national level remains the defining challenge.

Several pilot projects are exploring wireless EV charging while driving, where embedded roadway infrastructure transfers power to moving vehicles and could reduce reliance on large battery packs.

Foundational to Driverless Fleets

Wireless charging becomes architecturally essential for fully autonomous mobility, eliminating manual plug-in intervention, enabling high-utilisation fleet cycles, and redefining how depot energy logistics operate at scale.

These three vectors converge on a single strategic conclusion: wireless EV charging is not a product category. It is an energy interface layer embedded within transport infrastructure itself. Companies that control its core intellectual property will not merely sell products, they will shape the operating terms of electrified mobility.

The Market: From Pilot to Structured Growth

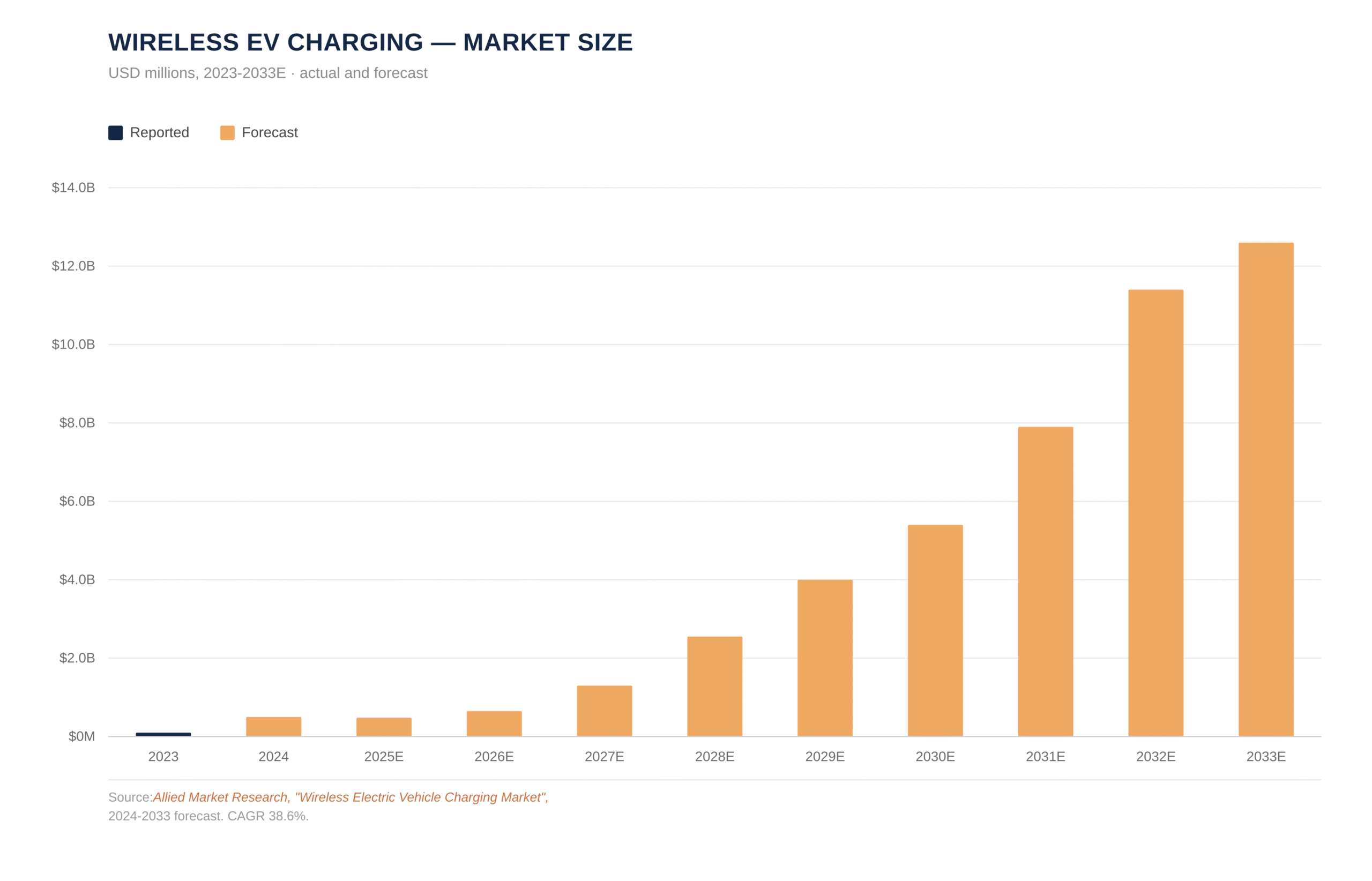

The wireless EV charging market was valued at $466 million in 2023. It is projected to reach $12.4 billion by 2033, growing at a CAGR of 38.6% over the decade among the steepest growth curves in the automotive technology sector. This figure captures the broader wireless power transfer ecosystem; estimates focused on the narrower static-pad segment run lower, but the directional consensus across research houses is unambiguous. As adoption increases, industry stakeholders are also evaluating wireless EV charging cost, balancing higher installation expenses against long-term operational efficiencies and reduced maintenance requirements.

Three validated demand drivers anchor the forecast. First, IEA projects EV sales could exceed 20 million units annually by 2025, sustaining the volume base that makes charging infrastructure investment commercially viable. Second, infrastructure investment programmes, the US Infrastructure Investment and Jobs Act, Europe’s AFIR regulation, and China’s state-directed EV build-out are channelling capital into next-generation charging at scale. Third, the formalisation of SAE J2954 (published October 2020 for light-duty vehicles, updated August 2024 with alignment systems) has reduced interoperability uncertainty that previously constrained OEM commitments. These technical benchmarks have significantly improved wireless EV charging efficiency, bringing performance closer to plug-in systems under properly aligned operating conditions.

Standards as Strategic Leverage

The SAE J2954 standard defines wireless power transfer at up to 11 kW for light-duty EVs, with efficiency of up to 93% at 10-inch ground clearance. Critically, it establishes the operating frequency band (81–90 kHz), coil topology specifications, and foreign object detection requirements. Companies whose patents read on these technical parameters hold standards-essential patent candidates, a qualitatively different competitive position from conventional portfolio accumulation.

The Patent Landscape: A Consolidating Arena

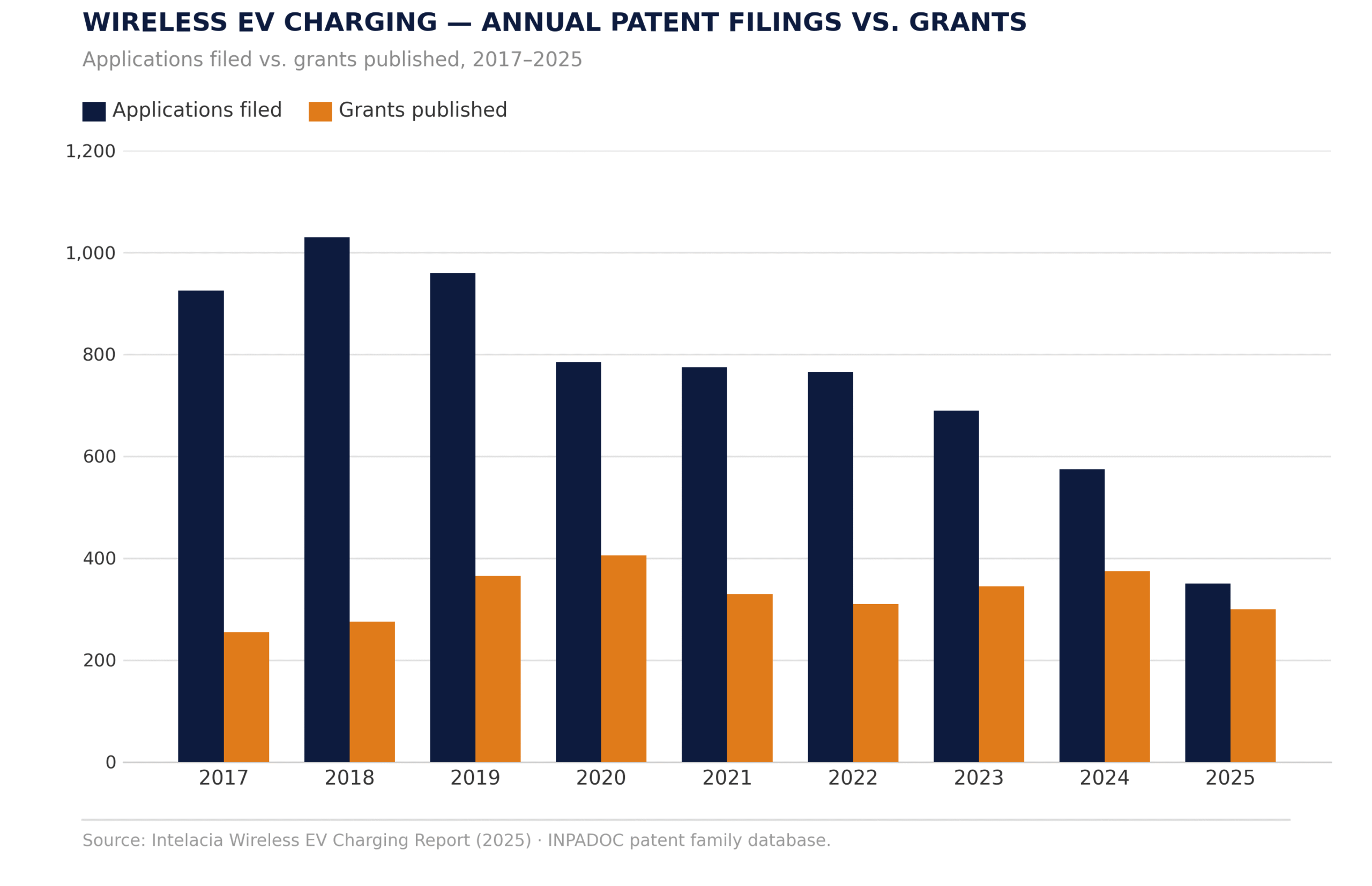

Analysis of the wireless EV charging patent database reveals a sector that peaked in filing volume in 2018 at 1,032 applications and has since undergone deliberate rationalisation, a pattern consistent with an infrastructure technology transitioning from exploratory R&D to commercial deployment. The cumulative decline from peak to 2024 is approximately 44%, interpreted not as retreat but as consolidation: dominant players are building density in high-value technology clusters rather than exploring breadth.

The grant trend carries its own signal. Grant publications peaked at 414 in 2020, reflecting maturation of the 2015–2017 filing wave and have remained structurally elevated through 2024 at 376 grants. This means the sector is converting substantial accumulated filings into enforceable rights at a steady rate, building an IP moat that will become increasingly relevant as commercialisation accelerates toward 2027–2030.

Who Controls the Technology: Assignee Intelligence

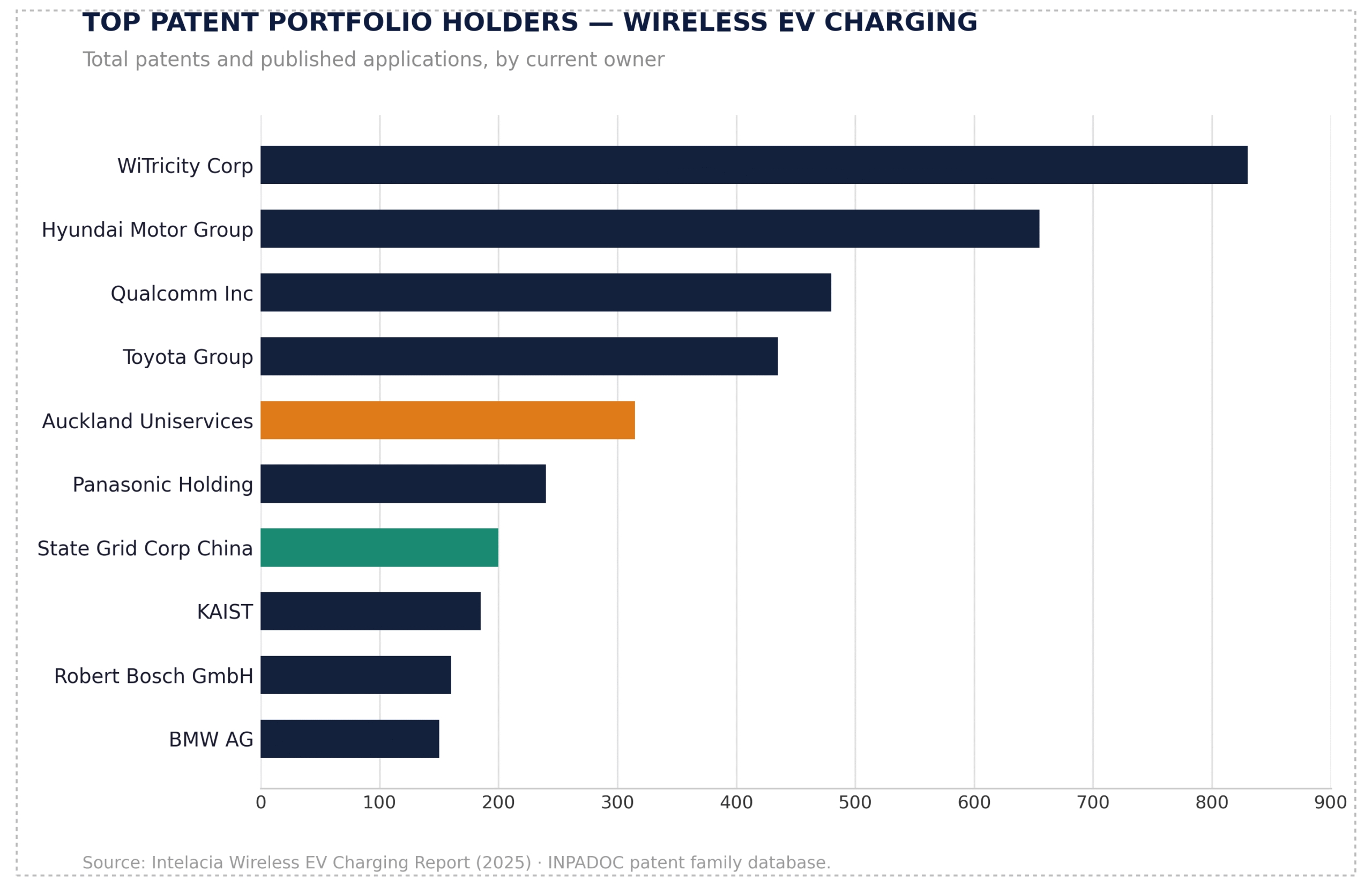

The competitive structure in wireless EV charging IP is unlike most automotive technology sectors. It is not dominated by automakers. It is dominated by technology licensors, specifically WiTricity Corporation, which leads decisively with 831 total patent records, followed by Hyundai Motor Group (658), Qualcomm (482), and Toyota Group (439). Leading wireless EV charging companies are increasingly competing through patent portfolios, licensing strategies, interoperability standards, and partnerships with global automotive manufacturers.

The presence of WiTricity and Qualcomm, pure-play technology companies with no vehicle manufacturing operations, at the apex of the IP hierarchy reflects a fundamental structural fact: foundational wireless power transfer technology was developed outside the automotive industry, and the patents controlling it are held accordingly. WiTricity’s portfolio traces to MIT research on resonant inductive coupling, commercialised from 2007 onward. Qualcomm’s wireless EV IP derived from Halo acquisition (2019), subsequently transferred to WiTricity.

Unlike plug-in charging, which is approaching commoditization, wireless charging remains patent-intensive, design-sensitive, and strategically fragmented. The real competitive shift is unfolding not in engineering labs but in IP portfolios, standards bodies, and licensing negotiations. The next generation of wireless EV platforms is expected to integrate seamlessly with autonomous mobility ecosystems, smart cities, and connected transportation infrastructure.

The OEM presence with Hyundai at 658, Toyota at 439 reflects a defensive integration strategy: automakers building portfolios to reduce licensing dependence on platform technology owners rather than to licence outward. The distinction matters enormously for competitive dynamics. WiTricity and Auckland Uniservices (318 records, commercialising University of Auckland’s foundational resonant transfer research) hold the IP that OEMs must navigate. Hyundai and Toyota hold the IP for vehicle-level integration that makes their own products defensible.

Geographic Competition: Where the IP Moat Is Being Built

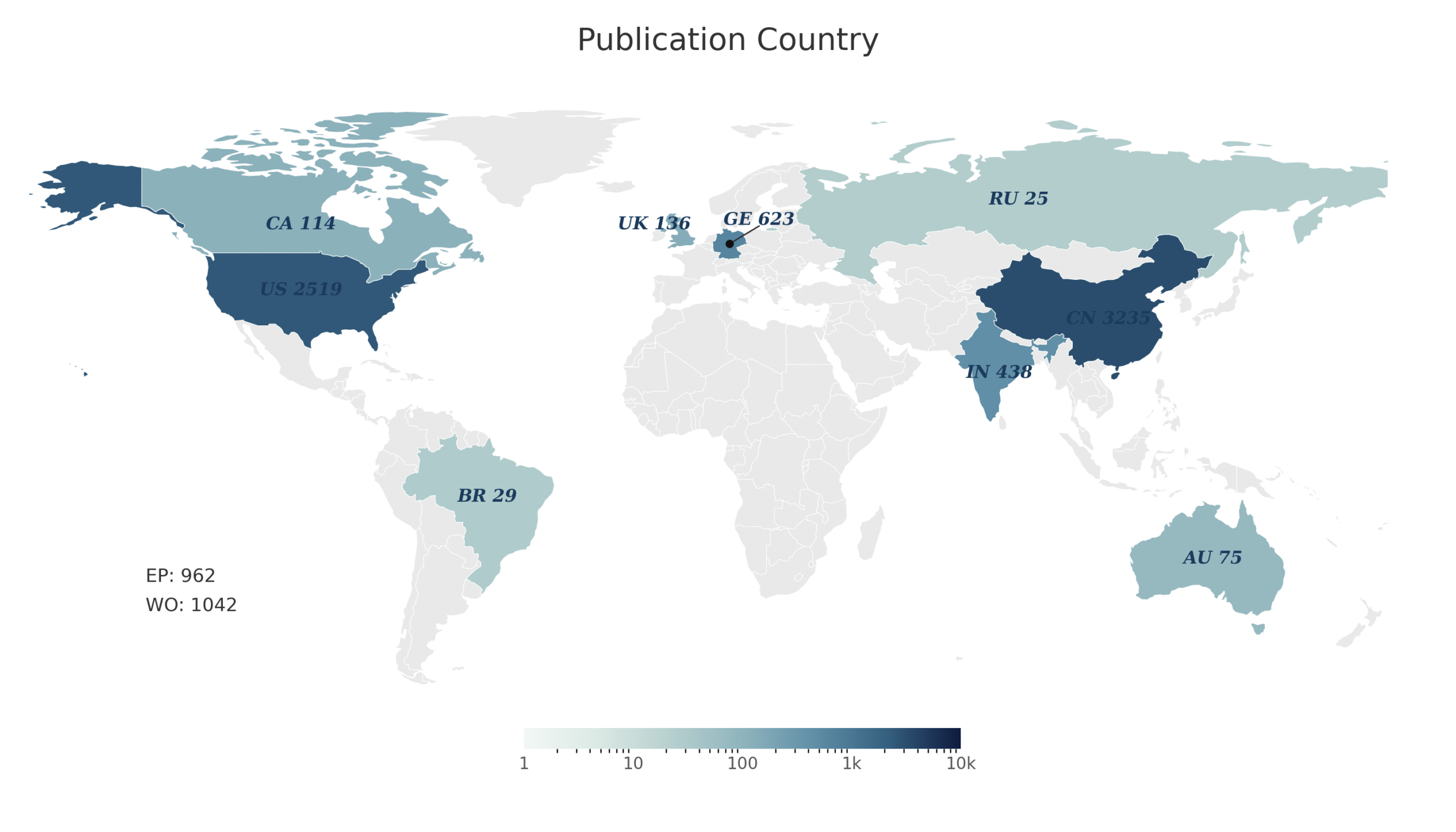

The jurisdictional data shows China (3,235 records) and the US (2,519 records) as the two dominant filing geographies, a pattern that mirrors the broader EV and autonomous vehicle IP race. The 1,042 PCT (WIPO) filings indicate that a significant proportion of filers are pursuing global protection strategies rather than confining their portfolios to domestic markets.

India’s position at 438 filings is analytically notable. India filings are led primarily by technology licensors, Qualcomm and WiTricity rather than OEMs, suggesting a forward-looking strategic positioning for emerging manufacturing and market growth rather than protection of existing commercial operations. This is a fundamentally different IP logic from China’s or South Korea’s filing patterns, where domestic industry participants drive volume.

The jurisdiction-specific time-to-grant data add a further layer of strategic complexity. France (33 months) and the US (35 months) offer the fastest paths to enforceable rights. Germany (74 months) and Russia (92 months) reflect the longest prosecution cycles. China (40 months), UK (40 months), South Korea (41 months), and Japan (43 months) cluster within a narrow three-month band indicating predictable mid-cycle timelines across the core industrial economies where deployment will ultimately matter most.

Quality Over Quantity: Where the Real Competitive Advantage Sits

Volume alone does not determine competitive strength in wireless EV charging IP. Analysis reveals a structural divide between technology licensors, WiTricity, Qualcomm, Auckland who hold high 360° portfolio quality at varying portfolio sizes, and OEM players Toyota, Hyundai who hold large volumes with comparatively lower quality scores. The quality metric incorporates citation strength, geographic coverage, legal status, and forward-looking applicability.

Strategic Implication for Late Entrants

Enforceable patent protection in wireless EV charging remains dense through the early 2030s, with larger expiry waves beginning post-2033. The window for securing foundational IP positions is narrowing. Companies entering after 2026 will face a significantly more constrained freedom-to-operate landscape and will increasingly need to navigate through licensing rather than building from scratch.

This quality gap has a direct commercial consequence. WiTricity’s business model is, in part, a licensing model, it has entered licensing agreements with major OEMs including BMW and has positioned its portfolio as standards-aligned. As SAE J2954 becomes the global benchmark, the patents that read on its technical specifications are transforming from ordinary IP assets into potential standards-essential patents carrying royalty obligations that every compliant device manufacturer must eventually address.

Strategic Outlook: Three Decisions That Will Define Leadership

The patent, market, and competitive data converge on three strategic imperatives for organisations navigating the wireless EV charging transition.

Engage the Standards Process or Pay to Participate Later

SAE J2954 sets the operating frequency, coil topology, EMF limits, and safety architecture for the global light-duty wireless charging market. Companies with patents reading on these specifications possess structurally superior IP positions. Those outside the standards process will face a landscape of mandatory licensing costs that their competitors helped to design. SAE TIR J2954/2 is already extending this dynamic into heavy-duty at 500 kW. The window for influencing the heavy-duty standard is open now.

Understand the Licensing Architecture Before Deploying

WiTricity’s multi-jurisdictional footprint, US 817, China 638, Japan 511, South Korea 419, India 406 covers the five largest automotive manufacturing and deployment markets simultaneously. Any OEM or tier-1 supplier building a wireless charging system without a licensing strategy aligned to that portfolio is accumulating risk quietly. The conversion wave from pending to granted patents between 2025 and 2030 will crystallise those risks into concrete enforcement exposure.

Position for Dynamic Charging Before Infrastructure Standards Lock In

Static pad-based systems dominate near-term commercial deployment, but dynamic in-road charging is where the long-term infrastructure platform value concentrates. Electreon’s in-road wireless charging pilots in Sweden, Italy, and Michigan represent early proof-points. The patents defining roadway integration, segmentation logic, and vehicle-infrastructure communication for dynamic systems are still being filed. This is the segment of the stack where a late mover can still influence the foundational IP landscape but that window is closing. Continued investment in wireless charging technologies and infrastructure standardization will determine how quickly the market transitions from demonstration projects to mainstream deployment.

Wireless EV charging is entering its infrastructural phase. The physics are established. The standards are publishing. The capital is scaling. What remains unresolved and therefore still strategically open is which companies, portfolios, and licensing arrangements will govern how the world’s electrified vehicles draw their power. The organisations making those decisions now will not merely participate in the next era of mobility. They will set its terms.

This article highlights only the strategic inflection points. Head to our website to explore the complete report, featuring a comprehensive analysis of the technology landscape, patent intelligence, competitive positioning, market dynamics, and strategic opportunities shaping the future of wireless EV charging.

Download Report

Download Report

Download Report

Download Report