The global rise of Ozempic and Wegovy has placed semaglutide at the center of both medical and commercial attention.

Developed by Novo Nordisk, the two therapies share the same underlying mechanism: a GLP-1 receptor agonist while targeting different indications: Ozempic for type 2 diabetes and Wegovy for obesity.

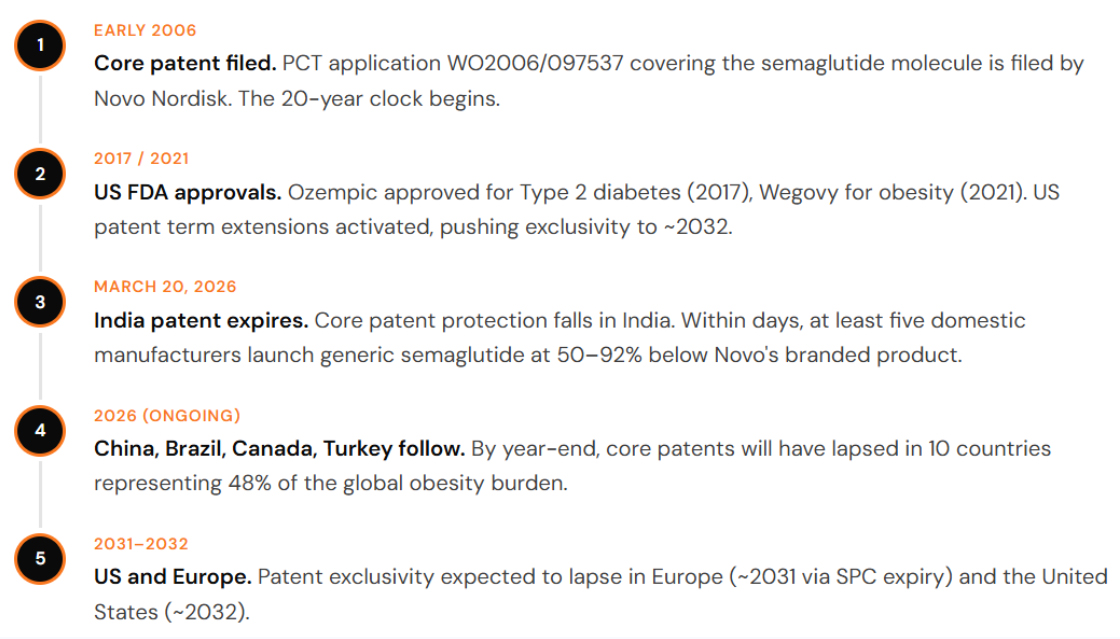

Beneath their market success lies a critical layer of protection: Novo Nordisk’s core patents covering the semaglutide molecule. These foundational patents, which support both products, are approaching expiry in several key jurisdictions, including China, India, and Brazil in 2026. In Canada, a corresponding core patent has already lapsed.

India: The Generic Avalanche

In India, generic versions launched immediately at up to 92% below branded prices. In the US, a political deal slashed Medicare costs by 71%. The drug is the same. The story is entirely different.

The core patent protecting semaglutide stems from PCT application WO2006/097537, filed in early 2006. Under standard patent law, the 20-year clock from that filing date runs out in early 2026 but not everywhere at once.

The reason for the geographic split is legal architecture, not chemistry. In the United States, Europe, and Japan, pharmaceutical innovators can apply for patent term extensions that compensate for the years spent in regulatory review before a drug reaches market. In the US, this extends semaglutide’s exclusivity to approximately 2032. In Europe, Supplementary Protection Certificates push loss of exclusivity to approximately 2031. In India, China, Brazil, Canada, and Turkey, no such extensions apply in the same way, meaning the core patent expired on schedule in early 2026.

The practical consequence is a bifurcated global market. Countries covering 40% of the world’s population and approximately 33% of global adults living with obesity have entered a generic semaglutide era. The remaining 60% primarily wealthy markets will wait up to six more years for that moment.

It is worth noting that the expiry of the core patent does not automatically clear the field. Novo Nordisk holds a portfolio of secondary patents covering formulations, delivery devices, and dosing regimens. In India, China, and Brazil, several generics companies are pursuing a “skinny label” strategy launching for indications not covered by any surviving secondary patent while challenging the rest through litigation. The road is open, but it is not unobstructed.

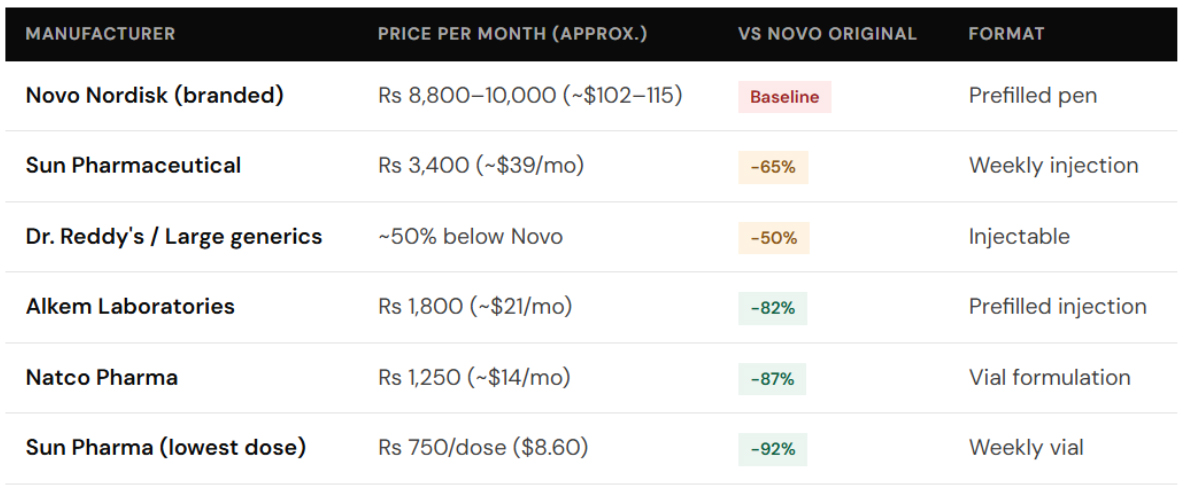

Following the weakening of semaglutide patent protection in India, multiple domestic manufacturers including Sun Pharmaceutical, Dr. Reddy’s Laboratories, Natco Pharma, and Alkem Laboratories have entered the market with significantly lower-priced alternatives to Ozempic. While larger players are offering products at roughly ~50% below Novo Nordisk’s original pricing, smaller manufacturers have pushed prices down by as much as ~80–90%, with the lowest-cost options representing a reduction of up to ~90% compared to pre-expiry branded levels.

The scale of mobilisation is significant. Following semaglutide’s patent expiry, more than 40 pharmaceutical companies in India are expected to launch over 50 distinct versions, reflecting one of the most aggressive competitive responses seen around a major patent cliff.

This intensity is underpinned by a substantial market opportunity. India has over 100 million people living with diabetes, alongside a rapidly growing population with high BMI. The GLP-1 receptor agonist market, valued at approximately $110 million in 2024, is projected to grow at a CAGR of over 34% through 2030.

With patent expiry and the entry of lower-cost alternatives, the market is now structurally positioned for rapid expansion, as affordability barriers decline and access broadens.

That observation identifies the most consequential long-run dynamic. India supplies approximately 20% of global off-patent medicines. Once semaglutide is manufactured at scale there, the commercial logic is that product will find its way to where demand is highest — including markets where the patent has not yet expired. Grey market channels, cross-border personal importation, and structured parallel trade will all apply pressure on Novo Nordisk’s pricing in patent-protected markets well before 2032.

Novo Nordisk’s response has been both rapid and strategic. The company reduced Wegovy prices in India by approximately 37% ahead of patent expiry, followed by further cuts of around 36% for Ozempic and 48% for Wegovy after generic competition intensified. Rather than competing purely on price, Novo appears to be repositioning its products around brand strength leveraging physician trust, clinical evidence, and established distribution to sustain a premium in a market where alternatives are priced significantly lower.

United States: Two Deals, One Drug, and a Price Still Too High for Most Americans

The push to lower semaglutide prices in the United States is primarily driven by a sharp rise in demand and the resulting strain on healthcare spending. Drugs like Ozempic have seen widespread adoption, particularly among Medicare beneficiaries, leading to billions of dollars in annual expenditure. Policymakers are increasingly under pressure to make these therapies more affordable for patients while ensuring the sustainability of public healthcare programs.

Under the Inflation Reduction Act, the government has begun using its position as a major purchaser to directly negotiate drug prices, aiming to secure meaningful discounts. At the same time, there is growing concern that, without intervention, expanding use of these drugs for conditions like obesity could significantly escalate long-term healthcare costs.

Together, these factors are driving a policy-led effort to reduce prices even in the absence of generic competition marking a shift from market-driven pricing to government-influenced cost control.

The first track is driven by the Inflation Reduction Act, which established a mechanism for the Centers for Medicare & Medicaid Services (CMS) to directly negotiate prices for high-cost drugs under Medicare Part D. Semaglutide products, including Ozempic and Rybelsus, were selected in the second round of negotiations. In November 2025, CMS announced a negotiated price of approximately $274 per month for these drugs, down from a list price of about $959 representing a reduction of roughly 70%. Higher-dose Wegovy was negotiated at around $385 per month. These negotiated prices are scheduled to take effect in January 2027 and will apply to Medicare beneficiaries, marking a significant policy-driven reduction in drug pricing despite continued patent protection.

The second track reflects a parallel pricing intervention emerging from the Trump administration’s policy approach. On November 6, 2025, a deal was announced with Novo Nordisk and Eli Lilly to reduce the cost of GLP-1 therapies, including Ozempic and Wegovy. Under this arrangement, prices for Medicare and Medicaid programs are expected to fall to approximately $245 per month, with patients facing co-pays of around $50. A direct-to-consumer channel is also being introduced, offering prices near $350 per month, with a projected decline toward $245 over time. The rollout is expected to begin with pilot programs in 2026, with broader implementation to follow. In exchange, manufacturers are receiving policy concessions, including tariff relief and commitments tied to domestic investment. While not a formal statutory framework like the Inflation Reduction Act, this approach reflects a parallel, negotiation-driven effort to compress prices creating uncertainty around how it will interact with the IRA’s negotiated pricing structure.

The interaction between the IRA-negotiated price (~$274) and emerging policy-driven pricing proposals creates a complex and evolving landscape. While the Inflation Reduction Act establishes a statutory, mandatory framework for price negotiation, other policy approaches such as international reference pricing models remain less formal and subject to implementation uncertainty. This creates potential ambiguity around how different pricing mechanisms may coexist or interact over time.

Despite this uncertainty, the broader political direction is clear. Drug pricing has become a central policy priority in the United States, and high-visibility therapies such as GLP-1 drugs are at the forefront of this debate. Even in the absence of generic competition, sustained policy pressure is already influencing pricing strategies and patient access pathways.

At the same time, expanded access particularly through potential Medicare coverage for obesity treatments introduces a volume dynamic that may partially offset pricing pressure. As access broadens, utilization is expected to increase, reshaping the revenue model for these therapies.

The longer-term implication lies beyond immediate pricing interventions. By the time patent protection begins to expire in the early 2030s, pricing expectations in the U.S. market may already be anchored by policy-driven benchmarks, fundamentally altering how generics compete when they eventually enter.

Five Tensions That Will Define the Next Five Years

The Ozempic story is almost always told in binary terms: innovator versus generic, expensive versus cheap, US versus India. The reality is considerably more complex.

- The leakage problem is not theoretical. The risk of cross-border leakage is not theoretical. As lower-cost semaglutide emerges, price differentials create incentives for grey channels, personal importation, and alternative supply routes. In the U.S., compounding pharmacies have already been active in producing GLP-1 formulations during shortages, highlighting regulatory gaps. While strict patent enforcement remains in place, these parallel pathways introduce indirect pricing pressure even before formal patent expiry.

- The biosimilar versus generic classification question is unresolved. Semaglutide is a synthetic peptide, placing it in a grey zone between traditional small-molecule generics and biologics. Where it is classified as a biosimilar, pharmacy substitution requires physician sign-off, slowing adoption. Where treated as a conventional generic, pharmacists can substitute freely. That classification varies by country and will materially affect how quickly generic semaglutide penetrates each market.

- The oral formulation changes the timeline. Rybelsus is already approved for diabetes, and both Novo Nordisk and Eli Lilly are advancing oral GLP-1 candidates for obesity. Oral formulations differ structurally from injectables both in manufacturing pathways and patent positioning. New formulations may carry fresh patent protection, potentially extending exclusivity even as injectable versions face increasing competition.

- The US pricing deals are legally fragile. Under the Inflation Reduction Act, negotiated drug pricing is a binding, statutory mechanism. However, broader pricing proposals such as international reference pricing models remain more fluid and politically contingent. This creates uncertainty around long-term pricing benchmarks. While policy is clearly pushing prices downward, the exact structure and durability of these mechanisms remain in flux.

- Quality and supply chain trust will determine adoption speed. Price is necessary but not sufficient to drive rapid generic substitution in a drug that millions take chronically. Quality failures contamination, dosing inconsistency, cold chain failures could slow generic adoption and preserve branded market share even where price parity exists

Conclusion

Novo Nordisk is entering a phase of structural pressure despite continued demand growth. While its semaglutide franchise has delivered exceptional expansion over recent years, the company has signalled moderating growth expectations as pricing pressure intensifies across markets. The underlying dynamic is clear: price compression is beginning to offset volume gains. In the United States, policy-driven pricing mechanisms are reducing realized revenue per unit, while in markets such as India, China, and Brazil, the expiry of core patents is enabling lower-cost competition.

Analysts estimate that Novo’s GLP-1 franchise has reached annual revenues in excess of $30 billion, placing it among the largest pharmaceutical product classes globally. However, future growth remains uncertain as competitive and pricing pressures increase.

Novo’s strategic response reflects a longer-term view. The company continues to invest in next-generation therapies, including oral semaglutide formulations for obesity and novel compounds such as Amycretin. The underlying thesis is that broader access to semaglutide driven in part by lower-cost alternatives will expand the overall GLP-1 market, creating a larger patient base for future differentiated therapies.