India’s intellectual property story in 2025 is one of striking paradox. By every filing metric, indian patent filings are on an extraordinary upward curve. Total patent applications rose to 1,43,729 patent filings in 2026 from 110,375 in 2024-2025, a 30% increase over the prior year with domestic patent application activity rising sharply by more than 44 percent, reaching 98,771 from 68,201. This surge reflects a growing culture of intellectual property awareness, increasing efforts to file patent assets, and a more proactive approach toward innovation within the Indian ecosystem.

India has moved, in a decade, from a passive participant in the global intellectual property system to one of its more active filers. The strengthening of the patent office infrastructure and faster patent prosecution timelines have contributed significantly to this growth.

And yet the harder question how much money are Indian companies making from the IP they own, yields a far less comfortable answer. IP monetization in India remains significantly underdeveloped. This gap is not a marginal inefficiency; it is a structural deficit at the centre of India’s innovation economy. Despite strong filing numbers and increasing patent search India activity, Indian companies continue to lose billions annually in unrealised licensing revenue, while paying substantially more to foreign rights-holders.

Understanding this gap, its causes, dimensions, and emerging solutions is central to evaluating the future of IP monetization in India.

The Numbers Behind the Gap

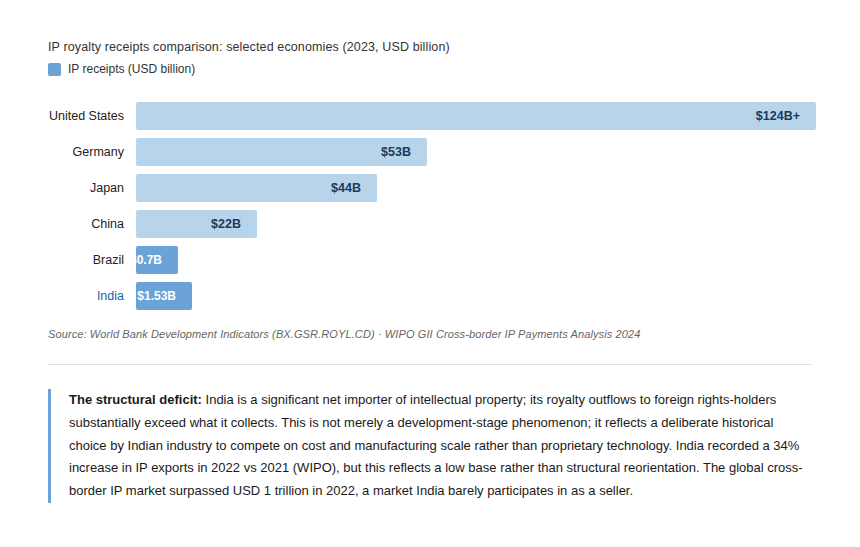

The most precise measure of IP monetization in India is its cross-border royalty and licensing account. According to global data, charges for the use of intellectual property receipts from licensing Indian-owned IP stood at approximately USD 1.53 billion in 2023. While this reflects some progress in IP valuation, it remains modest in global comparison.

In 2021, the United States alone received more than USD 124 billion in IP receipts over 80 times India’s figure. Germany received close to USD 60 billion. Even economies with fewer patent applications such as Brazil and Turkey show measurable licensing activity. India, despite strong patent filings in India, continues to underperform relative to its economic scale.

The outflow side reinforces this imbalance. India is a significant net importer of intellectual property, paying high royalties to foreign innovators. This imbalance reflects historical industrial strategies focused on cost competitiveness rather than proprietary indian patent ownership and monetization.

Recent growth trends such as a 34% increase in IP exports indicate progress. However, without stronger IP valuation frameworks, commercialization strategies, and licensing ecosystems, the gap in IP monetization in India remains structurally wide.

Why Indian Companies Have Not Monetized Their IP

The surge in patent application activity alongside weak monetization is not contradictory, it is systemic. To understand IP monetization in India, sector-specific analysis is critical.

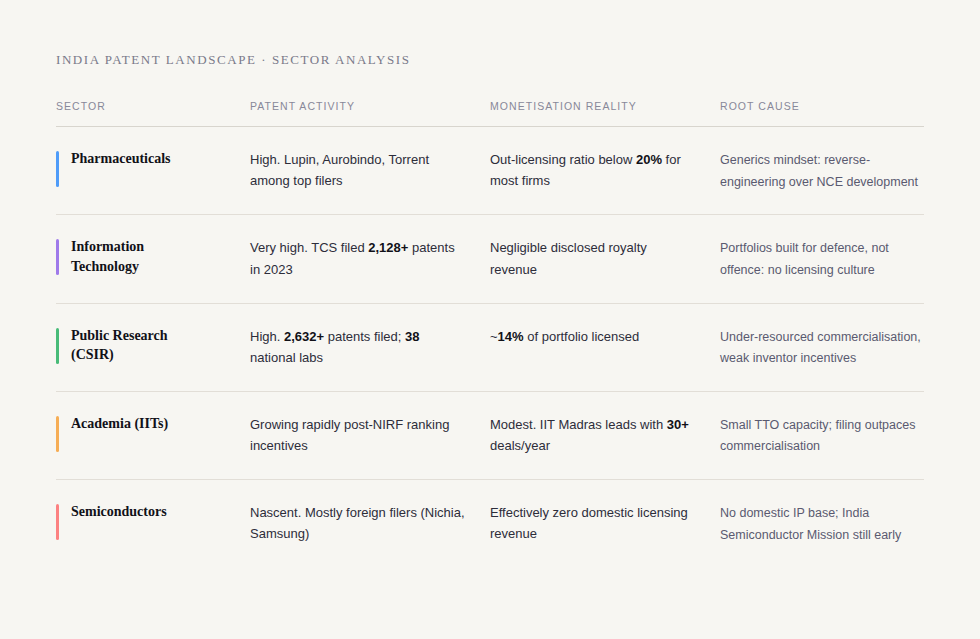

Pharmaceuticals: The Generics Trap.

India’s pharmaceutical sector has historically prioritized reverse engineering and process innovation. Companies focused on manufacturing efficiency rather than creating intellectual property assets designed for licensing. While this led to strong global generics leadership, it resulted in minimal royalty streams.

Even with increasing filings, the out-licensing ratio remains below 20%, compared to global innovators. The absence of structured IP valuation strategies and limited emphasis on patent filing for licensing purposes has constrained monetization.

Information Technology: Defence, Not Offence.

India’s technology sector has built substantial patent portfolios. CGPDTM data shows Computer Science and Electronics as the largest filing category in Indian patents. TCS, Infosys, HCL, and Wipro collectively hold tens of thousands of patents yet these portfolios are constructed almost entirely for defensive purposes: to shield client-facing solutions from litigation exposure in Western jurisdictions and to add credibility to enterprise sales pitches. There is no tradition in Indian IT of running IP as a profit centre in the way that IBM or Qualcomm have done. IBM historically generated USD 1–2 billion annually from patent licensing alone. No Indian IT company comes close to disclosing equivalent IP revenues.

The fundamental problem is strategic rather than capability based. Indian IT exports over USD 200 billion annually in services, but that revenue is structurally dependent on human capital deployment, not on proprietary technology licensing. The shift from a services model to an IP licensing model requires a different kind of R&D investment, a different risk appetite, and a different commercial function none of which the sector has yet built at scale.

India’s IT sector holds extensive intellectual property portfolios. However, these are largely defensive, used to protect operations rather than generate licensing revenue. Despite thousands of patent applications, companies rarely convert them into monetizable assets.

Unlike global leaders who treat IP as a revenue stream, Indian firms lack structured commercialization teams, licensing strategies, and dedicated patent prosecution approaches focused on monetization.

Public Research: The Utilisation Problem.

India’s public research institutions led by the Council of Scientific and Industrial Research (CSIR) with its network of 38 national laboratories represent a large and largely dormant patent portfolio. Despite a world-class research base, CSIR has managed to license only approximately 14% of its patent portfolio. The structural problem is compounded by resource constraints: IP commercialisation functions have historically been under-resourced, and budget pressures at individual labs have forced difficult trade-offs between filing new patents and commercialising existing ones. IITs face similar constraints, though IIT Madras has emerged as an exception its Technology Transfer Office has built a pipeline of over 30 active licensing deals annually, a model that other institutions are beginning to study.

Public institutions contribute significantly to patent filings in India, yet monetization remains weak. Only a small percentage of patents are licensed, reflecting limited commercialization capacity.

Even with strong patent search capabilities and research output, the absence of robust licensing infrastructure and underdeveloped IP valuation mechanisms restricts revenue generation.

The Enforcement Deterrent.

Until recently, the legal infrastructure for IP monetization was itself a material disincentive. Patent litigation in India was slow, expensive, and outcomes were uncertain. Licensing frameworks were poorly developed, royalty rate benchmarking was largely absent, and enforcement mechanisms were weak making the commercial conversion of patents a high-cost, low-certainty exercise. The Patents (Amendment) Rules, 2024 have addressed some procedural bottlenecks, reducing examination timelines and streamlining compliance, but their full effect is still working through the system.

Historically, weak enforcement discouraged IP monetization in India. Delays in the patent office, uncertainty in pre-grant opposition proceedings, and limited clarity in royalty frameworks reduced investor confidence. Recent reforms have improved efficiency, but stronger enforcement and faster dispute resolution remain essential to unlock full monetization potential.

Where India Is Beginning to Monetize

Despite systemic challenges, emerging examples demonstrate that IP monetization in India is possible when supported by strong innovation and commercialization strategies.

PHARMACEUTICAL & BIOTECH IP MONETIZATION

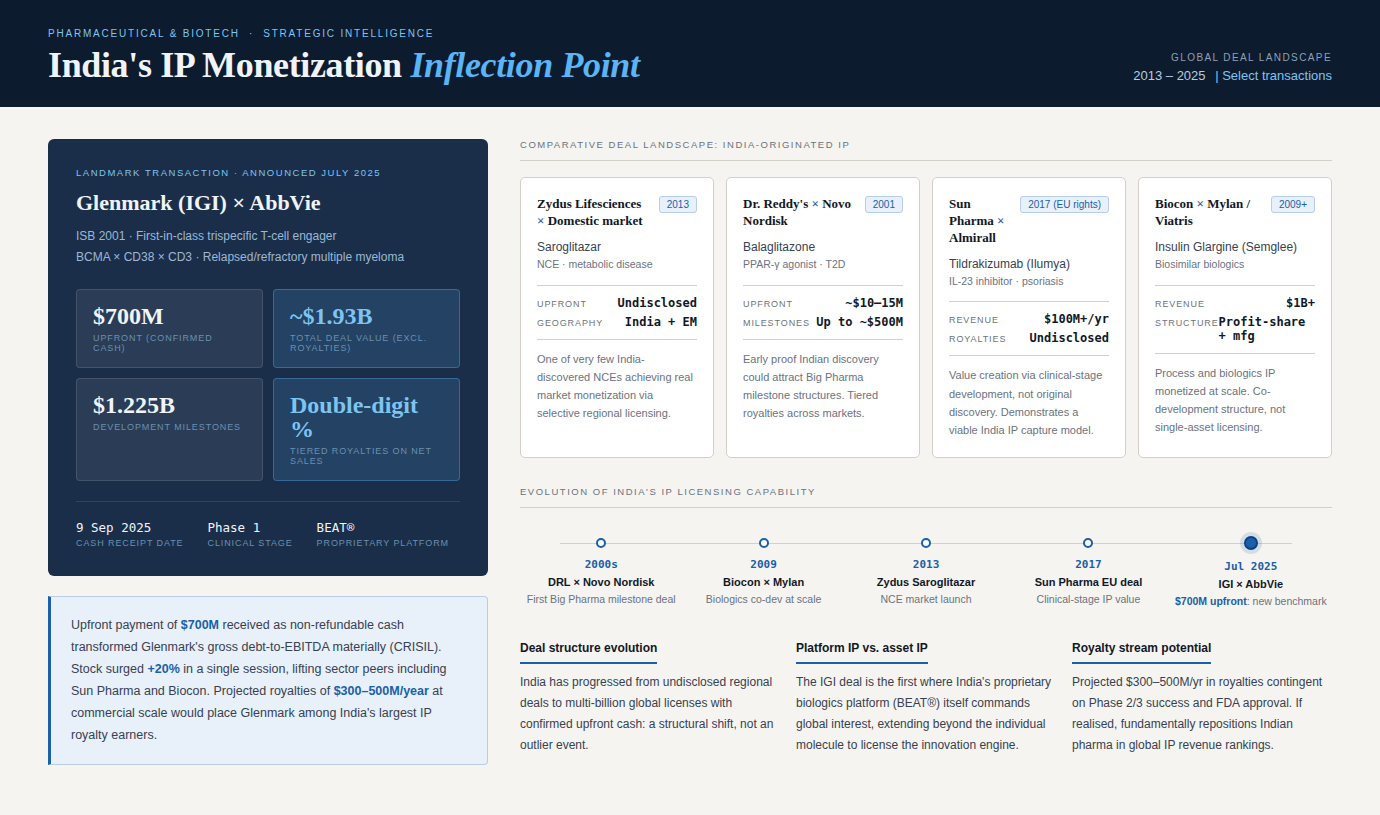

The Glenmark-AbbVie Transaction: A Structural Marker

Upfront: $700 million (confirmed cash)

Milestones: Up to $1.225 billion

Royalty: Double-digit

Total potential: ~$1.93 billion

This deal represents a landmark moment for IP monetization in India, showcasing how strong intellectual property combined with strategic licensing can generate global value.

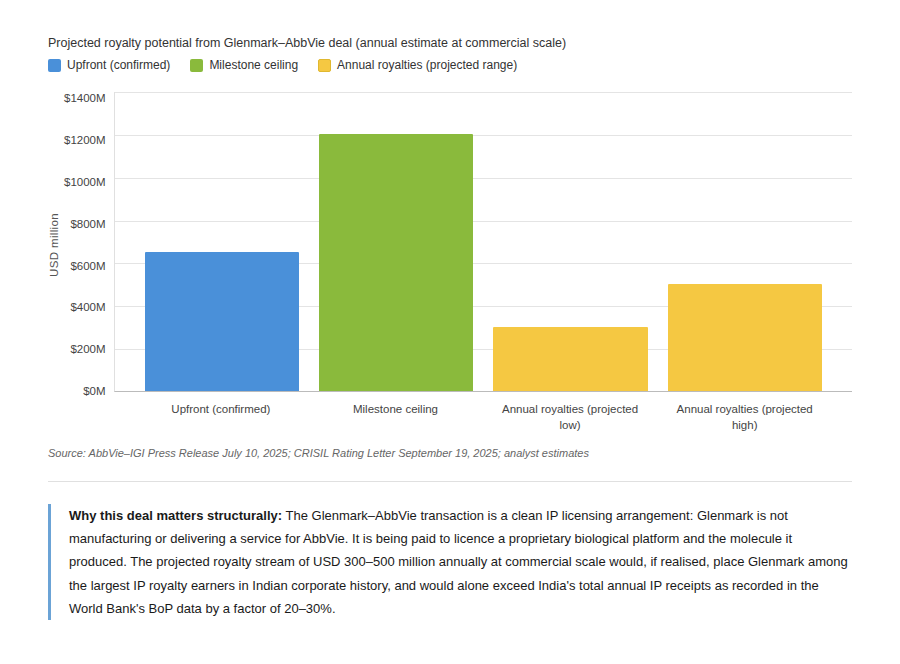

The most significant single data point in India’s IP monetization history arrived on 10 July 2025. Ichnos Glenmark Innovation (IGI), a subsidiary of Glenmark Pharmaceuticals, announced an exclusive licensing agreement with AbbVie for ISB 2001, a first-in-class trispecific T-cell engager targeting BCMA and CD38 on myeloma cells and CD3 on T cells, currently in Phase 1 clinical development for relapsed/refractory multiple myeloma, developed using IGI’s proprietary BEAT® protein platform. AbbVie agreed to pay a USD 700 million upfront payment, up to USD 1.2 billion in milestone payouts, and tiered double-digit royalties on net sales.

As confirmed by Glenmark to the stock exchanges, the USD 700 million upfront payment was received by IGI on 9 September 2025, a non-refundable payment that, per CRISIL’s assessment, transformed Glenmark’s financial risk profile materially, with gross debt to EBITDA expected to improve significantly. Multiple brokerages described this as the largest biotech licensing deal by an Indian company, sending Glenmark’s stock 20% higher in a single session and lifting peers including Sun Pharma and Biocon.

The projected royalty stream estimated at potentially USD 300–500 million annually at commercial scale would, if realised, place Glenmark among the largest IP royalty earners in Indian corporate history. Whether that outcome materialises depends on Phase 2 and 3 clinical trial results and eventual FDA approval, but the deal’s existence alone is a proof point that Indian innovation can generate globally competitive licensable assets.

Zydus Partnerships

Year: ~2013 (approval/launch phase; partnerships followed)

Original IP owner: Zydus Lifesciences

Licensees/Partners: Regional (largely undisclosed/publicly limited)

Economics: Not fully disclosed; revenue via India + emerging markets + selective licensing

Asset: Saroglitazar

Why it matters:

A rare example of an indian patent leading to commercial success through licensing and market expansion. One of the very few India-discovered NCEs with real market monetization

Sun Pharma–Tildrakizumab (Ilumya) licensing chain

Year (key licensing phase): 2017 (EU deal)

Original IP owner (nuanced): Early-stage molecule acquired, but clinical development + value creation by Sun Pharma

Licensee (EU): Almirall

Economics: Milestones + royalties (undisclosed)

Revenue signal: Global sales in hundreds of millions USD annually

Asset: Tildrakizumab

Why it matters:

Demonstrates how clinical-stage development and strategic patent filing can create monetizable assets. Shows India capturing value at clinical-stage IP development, even if not original discovery.

Dr. Reddy’s–Balaglitazone licensing deal

Indian IP owner: Dr. Reddy’s Laboratories

Licensee: Novo Nordisk

Deal economics (publicly reported ranges):

Upfront: ~$10–15 million

Milestones: Up to ~$500 million (widely cited range)

Royalties: Tiered

Asset: Balaglitazone

Signal:

An early indicator that Indian-origin patent application assets can attract global partnerships. Early proof that Indian discovery could attract Big Pharma milestone structures

Biocon–Insulin Glargine (Semglee) global partnership

Year (partnership evolution): 2009 onward (with Mylan → now Viatris)

Original IP owner: Biocon (process + development IP)

Structure: Co-development + global commercialization partnership

Economics: Profit-sharing + manufacturing revenues

Revenue signal: Biosimilars portfolio at $1B+ scale

Why it matters:

Highlights how process-based intellectual property can be monetized at scale through global collaboration. Process/biologics IP monetized at scale, not just one asset

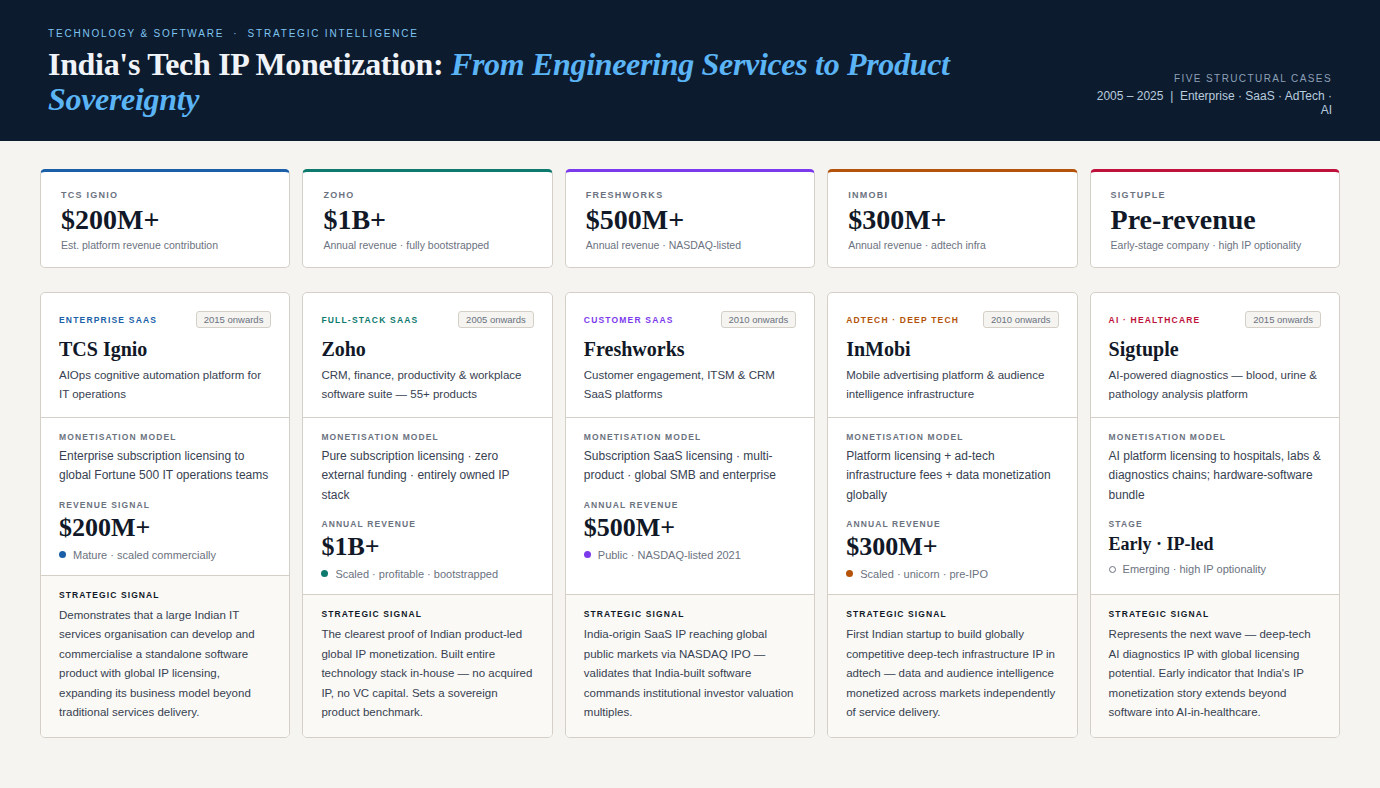

Top Indian IT & Deep Tech IP Monetization Signals

India’s technology sector is slowly transitioning toward product-led IP monetization in India.

- Enterprise platforms

- SaaS licensing models

- AI-based healthcare solutions

These examples reflect a shift from defensive patent filings in India toward revenue-generating IP assets.

- Tata Consultancy Services – Ignio Platform Licensing

Year: ~2015 onward (commercial scaling phase)

Original IP owner: TCS

Product/IP: Ignio (AIOps platform)

Monetization model: Enterprise software licensing (subscription-based)

Used by global clients for IT operations automation

Revenue signal: Multi-hundred million USD scale (platform-driven revenue within TCS portfolio)

Why it matters:

One of the few true enterprise software IP monetization cases from India

- Zoho Corporation – Full-stack SaaS Suite

Year: 2005–present (continuous IP build)

Original IP owner: Zoho

Monetization model: Subscription licensing (CRM, finance, workplace tools)

Revenue signal: $1B+ annual revenue (bootstrapped, IP-owned stack)

Why it matters:

Pure product-led IP monetization at global scale (rare in India)

- Freshworks – SaaS Platform Monetization

Year: 2010 onward

Original IP owner: Freshworks

Monetization model: Subscription SaaS licensing (customer engagement tools)

Revenue signal: $500M+ annual revenue

Why it matters:

Demonstrates India-origin software IP → global SaaS monetization

- InMobi – AdTech Platform IP

Year: 2010 onward

Original IP owner: InMobi

Monetization model: Platform licensing + ad-tech infrastructure monetization

Revenue signal: Hundreds of millions USD annually

Why it matters: Deep-tech infra (adtech + data) monetized globally

- Sigtuple – AI Diagnostics IP

Year: 2015 onward

Original IP owner: Sigtuple

Monetization model: AI platform licensing to hospitals/labs

Revenue signal: Early-stage (but strong IP-led model)

Why it matters:

Example of emerging deep-tech IP monetization (AI in healthcare)

Government Research

Modest but Real Progress. India’s publicly funded research ecosystem led by institutions like the Council of Scientific and Industrial Research (CSIR) and the IIT network has built one of the largest patent portfolios in the Global South. On paper, the numbers are impressive. CSIR alone has generated 14,000+ patents globally, spanning pharmaceuticals, materials science, chemicals, and engineering platforms.

But monetization tells a very different story.

Despite this scale, only ~9% of CSIR’s patents have been licensed. The remaining 90% sit uncommercialized protected, published, but economically inactive. Even among licensed technologies, value capture remains limited.

India’s public sector holds a vast repository of intellectual property, yet monetization remains limited. Despite thousands of patents, only a small fraction generates revenue. Improving IP valuation, licensing mechanisms, and commercialization support is essential to unlock this potential.

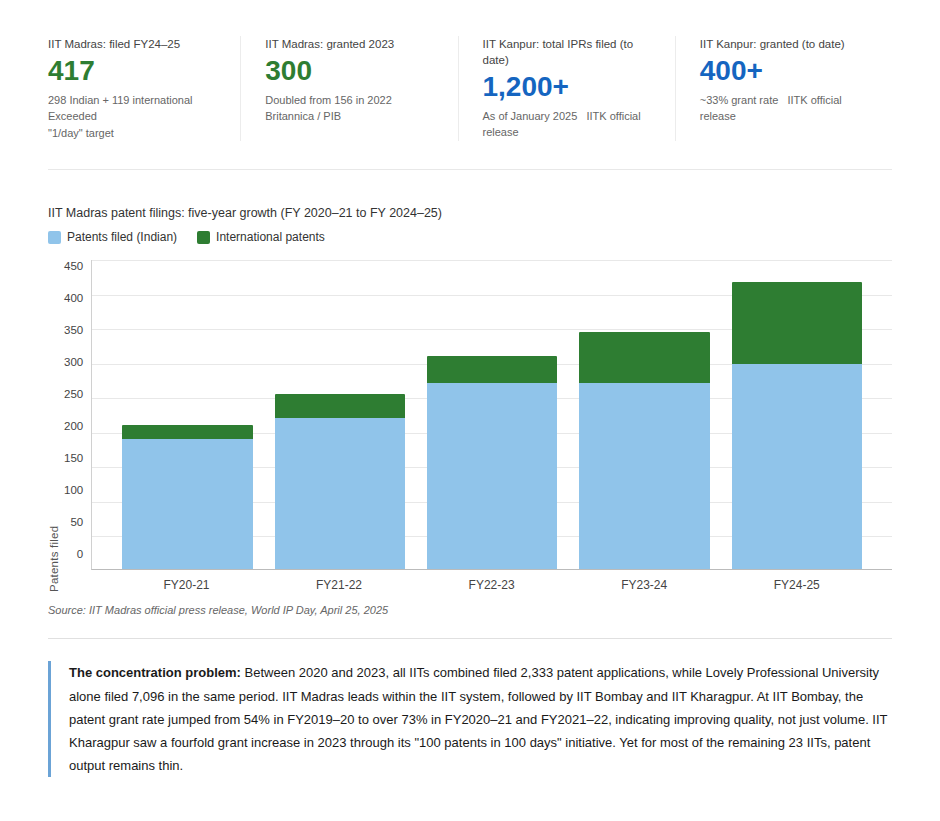

Educational Institutions

India’s IIT system has meaningfully accelerated patent output over the past five years. But the system-level numbers while impressive in isolation, conceal a significant structural problem: activity is highly concentrated in a handful of elite institutions, with the majority of India’s 23 IITs contributing modestly to the aggregate, while private universities file in volume without commensurate quality or commercialisation outcomes.

Filing a patent and commercialising it are two entirely different institutional capabilities. The technology transfer data from India’s best-performing academic institutions – IIT Madras and IIT Kanpur illustrates how wide the gap between creation and monetization remains, even at institutions that have deliberately invested in building transfer infrastructure

Academic institutions have increased patent application output significantly. However, commercialization remains concentrated in a few leading institutions.

While patent filings in India from universities are rising, the ability to convert these into licensing revenue is still developing.

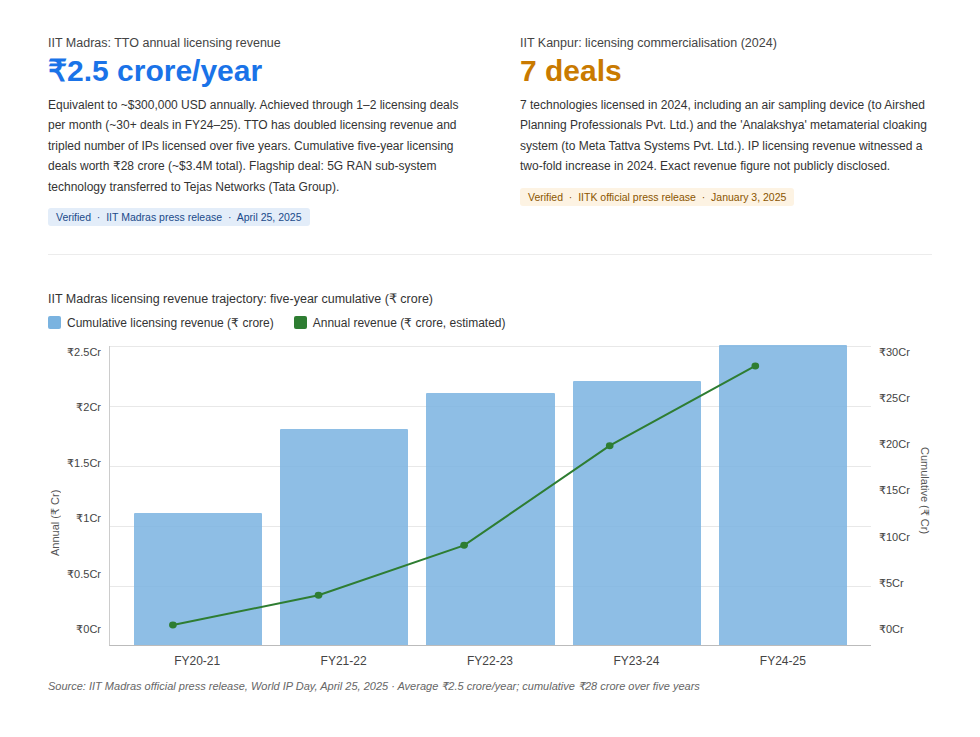

Licensing revenue: the real magnitude of the gap

Even where technology transfer occurs, the revenues generated reveal the true scale of India’s academic IP monetization challenge. The numbers from India’s best-performing institutions that have deliberately built licensing infrastructure show that annual licensing revenue is measured in crores, not hundreds of crores or thousands of crores. This is not a criticism of individual institutions; it is a structural observation about the ecosystem within which they operate.

Even among top institutions, licensing revenues remain modest. This highlights the structural challenge within IP monetization in India, where strong research output does not translate into financial returns.

The Structural Reforms That Could Change the Equation

India’s IP monetization gap is not primarily a filing problem the filing data makes clear the country can generate IP at scale. It is a commercialisation problem, a valuation problem, and in some respects a cultural problem within Indian corporate leadership.

To bridge the gap in IP monetization in India, several reforms are critical:

- Strengthening commercialization infrastructure

- Developing national IP marketplaces

- Enhancing patent office efficiency

- Improving pre-grant opposition clarity

- Encouraging strategic patent filing for licensing

India must also integrate better IP valuation practices and encourage companies to treat intellectual property as a core business asset. Participation in global standards and strengthening enforcement mechanisms will further enhance monetization outcomes.

Commercialisation infrastructure

India needs government-backed IP marketplaces and licensing intermediaries to connect patent holders particularly CSIR laboratories and IITs with potential licensees who lack discovery mechanisms to find them. The US Bayh-Dole Act of 1980, which allowed universities to retain ownership of federally funded research and commercialise it through licensing, is the most empirically validated model for converting public research into private licensing revenue. India’s equivalent framework remains structurally underdeveloped. The contrast is stark: IIT Madras’s Technology Transfer Office has built a pipeline of 30+ licensing deals annually through institutional investment other institutions have yet to build comparable capacity.

IT sector reorientation from defence to offence

Indian IT companies with large patent portfolios need a conscious strategic reorientation. The global cross-border IP market exceeded USD 1 trillion in 2022, growing at approximately 5.5% per year, a market India’s software-intensive firms are almost entirely absent from as sellers. Building even modest licensing revenue in AI inference architectures, cloud optimisation, and enterprise software, areas where Indian firms have genuine depth would represent a structural addition to the current services-revenue model. IBM’s historical USD 1–2 billion annual patent licensing revenue was not accidental; it required an explicit decision to treat IP as a business unit.

Standard Essential Patent participation

As India becomes a larger market for 5G, AI-embedded devices, and connected vehicles, the royalties flowing to SEP holders will be material. Indian companies are currently almost entirely absent from the standard-setting bodies, IEEE, ETSI, 3GPP that determine whose patents become standard-essential. SEP royalties are among the most predictable and durable in the IP ecosystem. Participation requires long-term commitment and R&D investment in standards-relevant technology, but the structural returns are compounding. This is a 10-year strategic priority and the time to begin is now.

Conclusion: The Distance Between Filing and Earning

India’s IP trajectory in 2025 is genuinely impressive at the level of inputs. With total IP filings rising and domestic patent applicants now in the majority for the first time, the country’s innovation culture is real and growing. The Glenmark-AbbVie transaction demonstrates that the outputs of that innovation can, when properly developed and commercially structured, attract billion-dollar valuations from the world’s most sophisticated pharmaceutical acquirers.

But one landmark deal does not constitute a monetization economy. The distance between India’s filing volume and its royalty receipts measured in the tens of billions of dollars against peer economies is the clearest indication that the country has not yet built the commercial infrastructure, the legal confidence, or the strategic orientation necessary to convert its IP creation into IP earnings at scale. The filing paradox will persist until Indian companies, institutions, and policymakers treat IP not as a protection mechanism or a compliance exercise, but as a business one that requires investment in valuation, deal structuring, enforcement, and the commercial disciplines that turn patents into revenue.

India’s IP story is no longer constrained by its ability to invent, but by its ability to convert invention into sustained, system-level value and until that monetization architecture scales, innovation will remain an underleveraged asset rather than a compounding economic force.