There is a quiet land grab underway, one measured not in acres, but in data points, APIs, and farmer logins. The companies winning this race are not necessarily selling the best seeds or the most effective herbicides. They are selling something more durable: a new generation of AgTech platforms, which gives them the ability to sit between a farmer and every decision they make.

For most of history, the key assets were tangible: soil, seed, chemical. Now a new asset class is emerging, one invisible to the naked eye but potentially more valuable than any of the above: the farmer’s decision interface. Whoever owns the screen where a farmer plans their season, orders inputs, and monitors their crop is effectively building a Farm Operating System (Farm OS), a platform with compounding advantages that will be nearly impossible to dislodge. Precision agriculture has accelerated this shift by transforming farming into a data-inte nsive enterprise.

Why AgTech platforms, not products, are now the prize

The logic is straightforward and drawn from a playbook refined in every other industry digital technology has touched. Once a farmer routes their field boundaries, soil data, crop history, and equipment logs through a single platform, switching costs become enormous. The more seasons of data a platform accumulates, the more accurate its yield predictions; the more accurate its predictions, the more the farmer relies on it; the more the farmer relies on it, the less likely they are to leave. This is the classic platform flywheel and it is now spinning inside agriculture.

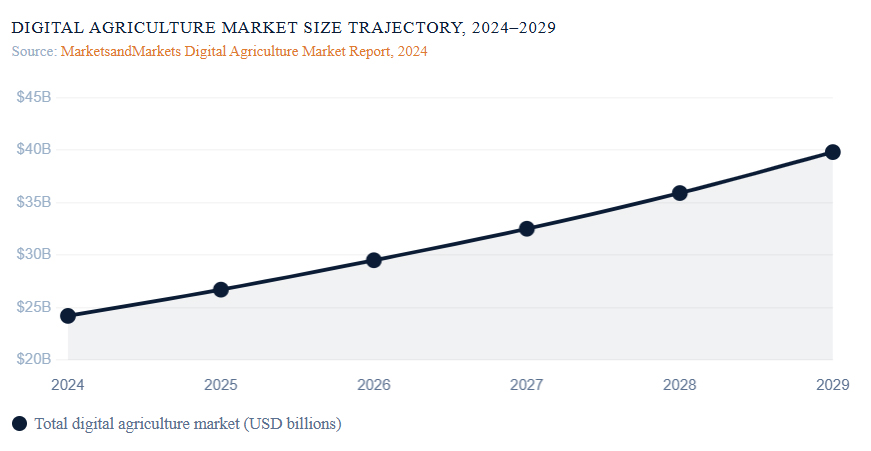

McKinsey has estimated that digital technology could add up to $500 billion to global GDP by 2030, with farming described as “the least digitised industry in the world.” That gap between current digitisation and potential represents the market that platform companies are now competing to fill. At the center of this transformation is precision farming, where data from machinery, sensors, satellites, drones, and agronomic models is used to optimize field-level decisions, making digital platforms increasingly indispensable to modern farm operations

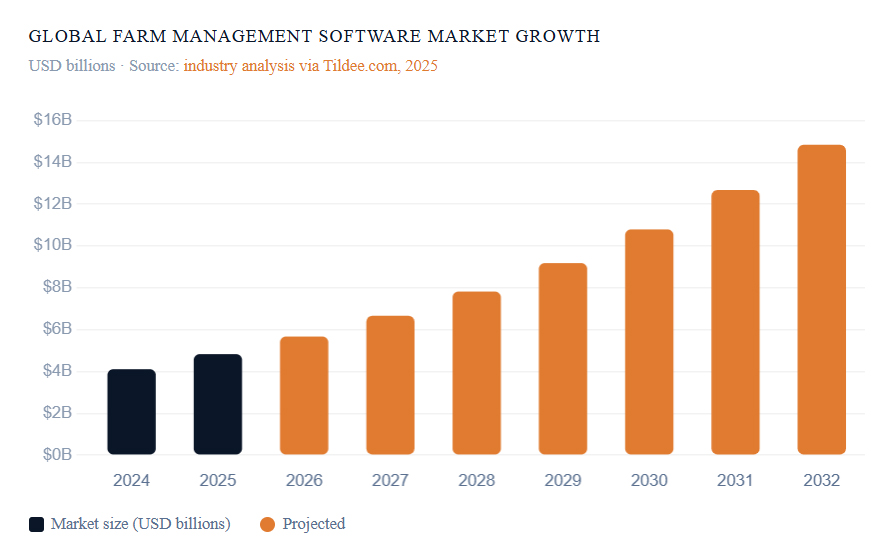

Farm management software, the core of the farm OS illustrates the opportunity most concretely. According to industry analysis, the global farm management software market is expected to rise from $4.1 billion in 2024 to $14.8 billion by 2032, a 17.4% CAGR well above the digital agriculture market average.

The four armies competing for the farmer’s screen

The competitors converging on this space arrive from very different starting positions which makes the battle all the more interesting. Equipment manufacturers bring hardware integration. Crop science companies bring agronomic trust. Data platforms bring intelligence infrastructure. And governments, particularly in emerging markets, are entering the arena with national platforms that could set the rules for everyone else.

John Deere Operations Center

HARDWARE-LED

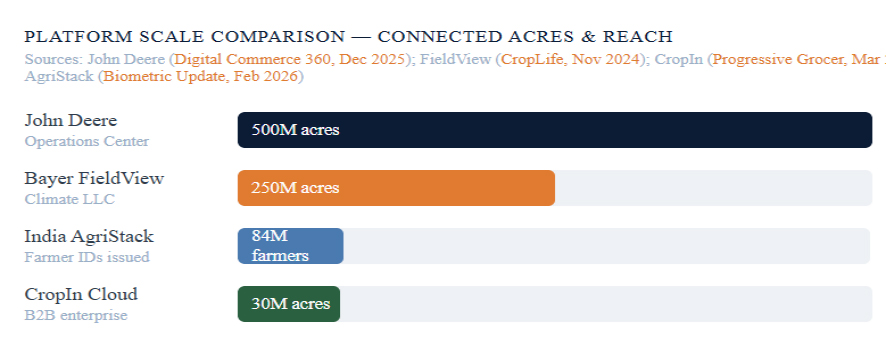

John Deere is the most powerful player in this war, and not primarily because of software. It is powerful because it sells the machines, and the machines generate the data. As of December 2025, Deere reported more than 1 million connected machines in operation and its Operations Center platform covering 500 million engaged acres globally with a stated target of 600 million by 2030.

The strategy is layered. Every new 8R and 9R series tractor is built “Autonomy Ready,” requiring only perception hardware to become fully autonomous. A retrofit programme extends this to tractors built as far back as mid-2020, turning each upgraded machine into a data-generating node in the Operations Center network with a recurring subscription revenue attached. John Deere’s See & Spray technology, integrated with Operations Center, achieved a 59% average herbicide reduction across 1 million acres in 2024 delivering $15.70 in savings per acre. When a platform demonstrably saves money, the farmer becomes deeply resistant to leaving it.

Bayer Climate FieldView

CROP SCIENCE-LED

Climate FieldView, the flagship product of Climate LLC, Bayer’s digital farming arm is now available in 23 countries on more than 250 million subscribed acres as of late 2024. In the United States, its subscribed acres represent more than half of all corn, soybean and cotton acres planted.

The business logic is transparent and elegant: FieldView’s job is not primarily to sell software subscriptions. Its job is to generate agronomic prescriptions that recommend Bayer seeds Dekalb, Asgrow and Bayer crop protection products. The platform’s 2025 strategy focuses on growing variable-rate prescription adoption, building a digital soil health layer, and expanding integration with independent agronomists. Every prescription generated is a nudge toward a Bayer product. The platform is, in effect, the world’s most sophisticated sales tool one that the farmer pays for and trusts because it appears to be on their side.

The recent integration between FieldView and John Deere Operations Center announced in February 2026 illustrates how platform ecosystems can interlock rather than purely compete. Farmers can now transfer FieldView prescriptions wirelessly to Operations Center for execution, without thumb drives. Both platforms expand their utility; both tighten the farmer’s dependence on the ecosystem as a whole.

CropIn Cloud

DATA INFRASTRUCTURE-LED

200M+ acres across 103 countries. A pure-play agriculture cloud with 500 crops, 10,000 varieties in its knowledge graph designed to serve agri-businesses, banks, and insurers rather than individual farmers directly.

Its 2025 partnerships tell the story: a strategic deployment with Walmart to optimise fresh produce supply chain forecasting; a regenerative agriculture rollout with EIT Food across Europe; strategic alliances with Wipro and BCG. CropIn is positioning itself as the intelligence layer that global food corporations and institutional agri-lenders plug into.

India AgriStack (DAM)

GOVERNMENT-LED

India’s Digital Agriculture Mission, approved in September 2024 with a budget of Rs 2,817 crore (approximately $340 million), represents something qualitatively different from a startup or corporate platform play. It is a sovereign attempt to build Digital Public Infrastructure for agriculture, the agricultural equivalent of what UPI did for payments.

AgriStack rests on three federated registries. A Farmer Registry assigns each farmer a unique digital Farmer ID with 84 million IDs already generated as of early 2026. A Geo-Referenced Village Map Registry links farmland to precise coordinates. A Crop Sown Registry captures what is actually in the ground, season by season with 253 million plots mapped during the 2024-25 Rabi season alone.

India AgriStack: scale of implementation

Sept 2024

Digital Agriculture Mission approved with Rs 2,817 crore budget. AgriStack designated as the foundational Digital Public Infrastructure layer.

Dec 2024

Digital Crop Survey operational in 17 states, 492 districts, and 421,000 villages. 253 million farm plots mapped during Rabi 2024-25 season.

Early 2026

84 million Farmer IDs generated across 19 states. Target: 110 million farmers and 300 million plots by Kharif 2026.

2027 target

Full geo-referencing of all agricultural land parcels. Open API gateway (UFSI) to enable private agri-tech platforms to build on top of the public data layer.

What makes AgriStack strategically significant is not just its scale, but its architecture. The Unified Farmer Service Interface, an open API gateway is designed to let authorised public and private applications access farmer data with consent.

The implications for the private platform war are profound. If AgriStack achieves its ambitions, private platforms in India will no longer be competing to build the foundational farmer data layer, that layer will already exist, owned by no single company. Competition will shift upward, to the quality of applications and recommendations built on top of a shared data commons. It is a fundamentally different model from the walled garden approach pursued by Deere or Bayer in the West.

The data ownership question that changes everything

Beneath the platform competition lies a more fundamental question that agriculture has not yet resolved: who owns the data that flows from a farm? Every connected tractor, every soil sensor, every satellite pass over a field generates data that is simultaneously the farmer’s property, the platform’s raw material, and potentially a public interest asset.

Platform companies have been careful to assert farmer data ownership in their marketing. Bayer states that farmers can request deletion of their individual data at any time. John Deere’s Operations Center provides export functionality. But as Civil Eats reported in 2026, watchdog groups warn that terms buried in long contracts may grant broader rights over anonymised and aggregated data pools which are, arguably, the most valuable data assets of all. A company that knows the average yield of every field in Iowa, correlated with every input applied, holds something extraordinary regardless of what any individual farmer can delete.

This is the strategic core of the platform war. The companies building farm operating systems are not primarily competing to sell software subscriptions. They are competing to accumulate the largest, richest, most granular agricultural dataset in the world — one that will power the next generation of AI-driven recommendations, input pricing, land valuation, and supply-chain optimisation. The farmer’s decision interface is the entry point. The dataset is the destination.

The road ahead: consolidation and convergence

The current landscape with hardware giants, crop science companies, agriculture technology (AgTech) companies, pure-play data platforms, and governments all competing for the farmer’s screen is almost certainly a transitional state. Platform economics historically produce consolidation around one or two dominant ecosystems, with a long tail of specialists surviving in niches the dominant platforms cannot profitably serve.

Several dynamics will determine the final configuration. In developed markets, the integration between equipment and software gives Deere a structural advantage that will be difficult to overcome. In emerging markets with large smallholder populations, government-led DPI models like India’s AgriStack may set the terms for everyone else. In the enterprise agri-business segment, intelligence infrastructure providers like CropIn may find that they don’t need to win the farmer relationship at all, only the B2B relationships that sit above it.

What is certain is that the outcome of the farm OS battle will shape agriculture far beyond software subscriptions. The platform that becomes the dominant decision interface for global farming will influence which seeds are recommended, which fertilisers are prescribed, which practices are rewarded and which are quietly discouraged. In a world increasingly shaped by climate change, these decisions will also affect how agriculture manages emissions, conserves resources, and adapts to environmental uncertainty. The stakes, in other words, are not merely commercial. They are agronomic, environmental, and ultimately political.

The seed companies understood this first. The ag tech companies understood it next. Governments are only now beginning to grasp it. The rest of the world should probably start paying closer attention.