Sprayable double-stranded RNA (dsRNA) has crossed from lab curiosity to registered product. With the EPA’s 2023 approval of the world’s first foliar dsRNA biopesticide, and Bayer, Syngenta, Corteva, BASF and FMC all building positions, the underlying patent landscape is shifting fast but it remains more open than almost any other input-technology category in agriculture, creating a real window for freedom-to-operate (FTO) and white-space strategy.

The rapid evolution of RNAi biopesticides is also accelerating interest in RNA based biopesticides for sustainable crop protection, as researchers and industry stakeholders seek targeted alternatives that reduce environmental impact while maintaining high pest-control efficacy.

Why this is the inflection point

RNA interference has been a tool in molecular biology since the early 2000s, and a target for ag-biotech patenting since at least the early 2010s. What’s changed is regulatory proof-of-concept.

RNAi-based crop protection splits into two technical families.

From a technical perspective, RNAi based pest control production application and the fate of DSRNA remain critical research areas, with scientists evaluating manufacturing scalability, field deployment methods, environmental persistence, and degradation pathways to optimize commercial performance.

- Plant-incorporated protectants (PIPs): Scientists genetically engineer crops to produce double-stranded RNA (dsRNA) inside the plant. When a pest feeds on the plant, this dsRNA triggers the pest’s RNA interference (RNAi) system, shutting down essential genes. This is the approach used in Bayer’s corn rootworm traits.

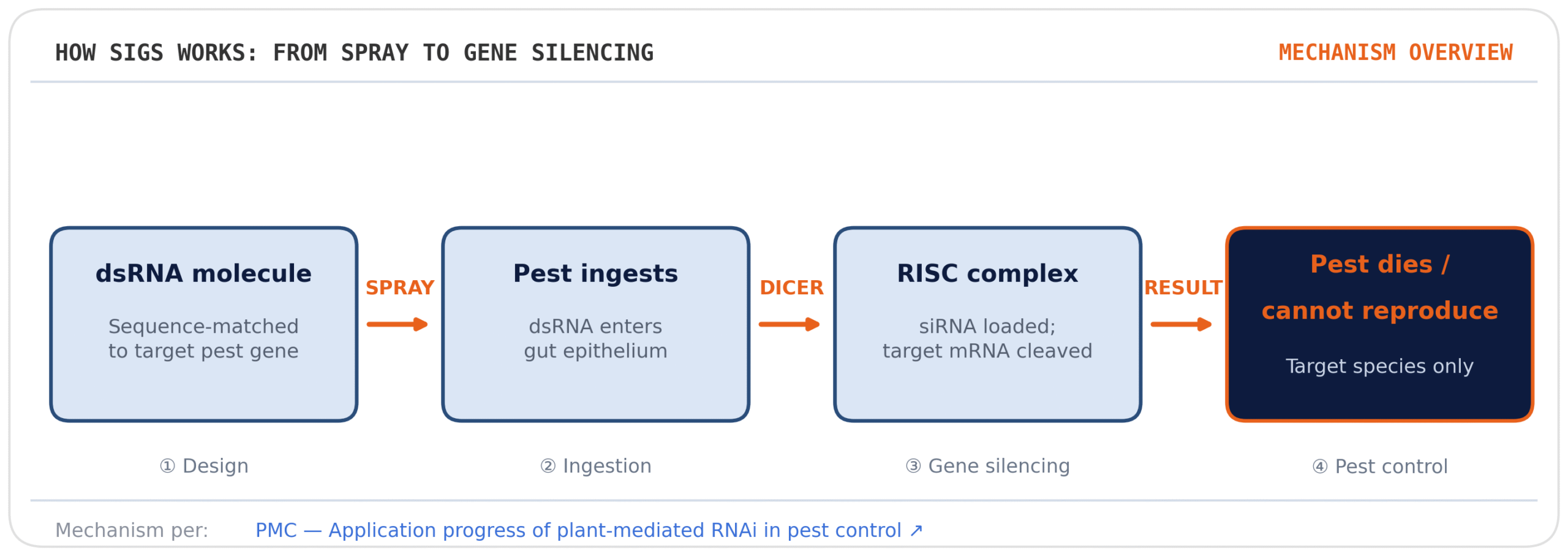

- Spray-induced gene silencing (SIGS): Instead of modifying the plant, dsRNA is sprayed onto crops like a conventional pesticide or fungicide. The sprayed RNA is designed to specifically match an essential gene in a target pest. When the pest ingests it, its own RNAi machinery switches off that gene, preventing the production of proteins required for survival.

The non-PIP route is the one reshaping the IP landscape, because it sidesteps much of the regulatory and public-perception baggage attached to genetically modified crops while still being protectable as composition-of-matter, sequence, formulation, and method-of-use IP. In December 2023, the EPA registered Ledprona, the active ingredient in GreenLight Biosciences’ Calantha™, as the world’s first sprayable dsRNA biopesticide targeting the Colorado potato beetle, one of the most resistance-prone pests in North American agriculture.

That precedent matters enormously for IP strategy. A regulator-tested pathway de-risks the entire category: it tells every agrochemical major and ag-biotech startup that a SIGS product can move from greenhouse to field to registered SKU using existing statutory machinery, rather than waiting on bespoke rulemaking.

Within a year of Ledprona’s registration, two further RNAi active ingredients provisionally named Galquin and Vadescana had already received ISO common names, a strong signal that a fast-following pipeline of SIGS actives is now moving through development, each one a potential anchor for a fresh patent family covering target sequence, formulation, and application method.

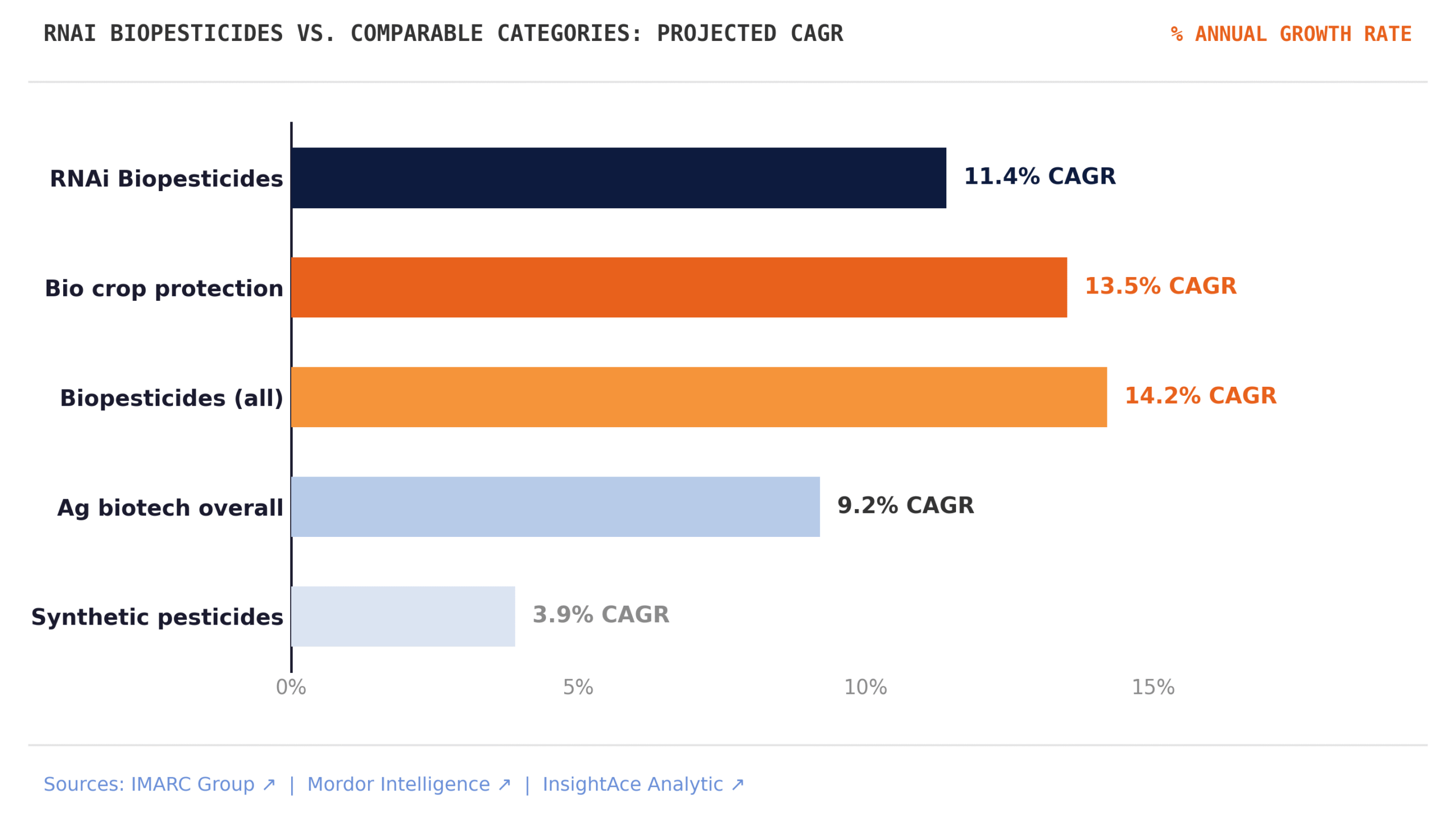

Market sizing: small base, steep curve

Independent analysts converge on a similar starting point, a market still measured in low single-digit billions but diverge on how steep the next decade’s growth curve is, which itself is informative.

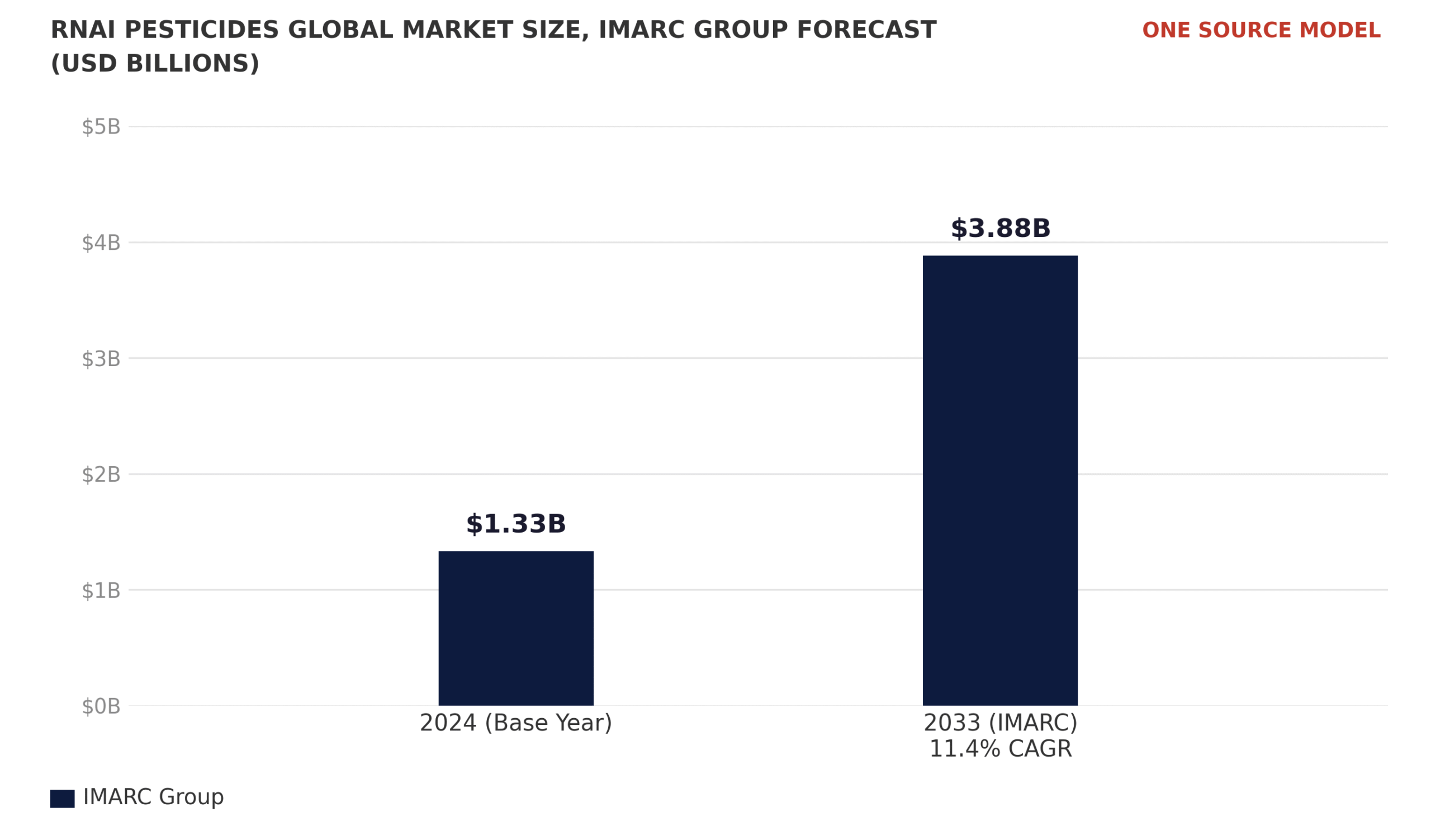

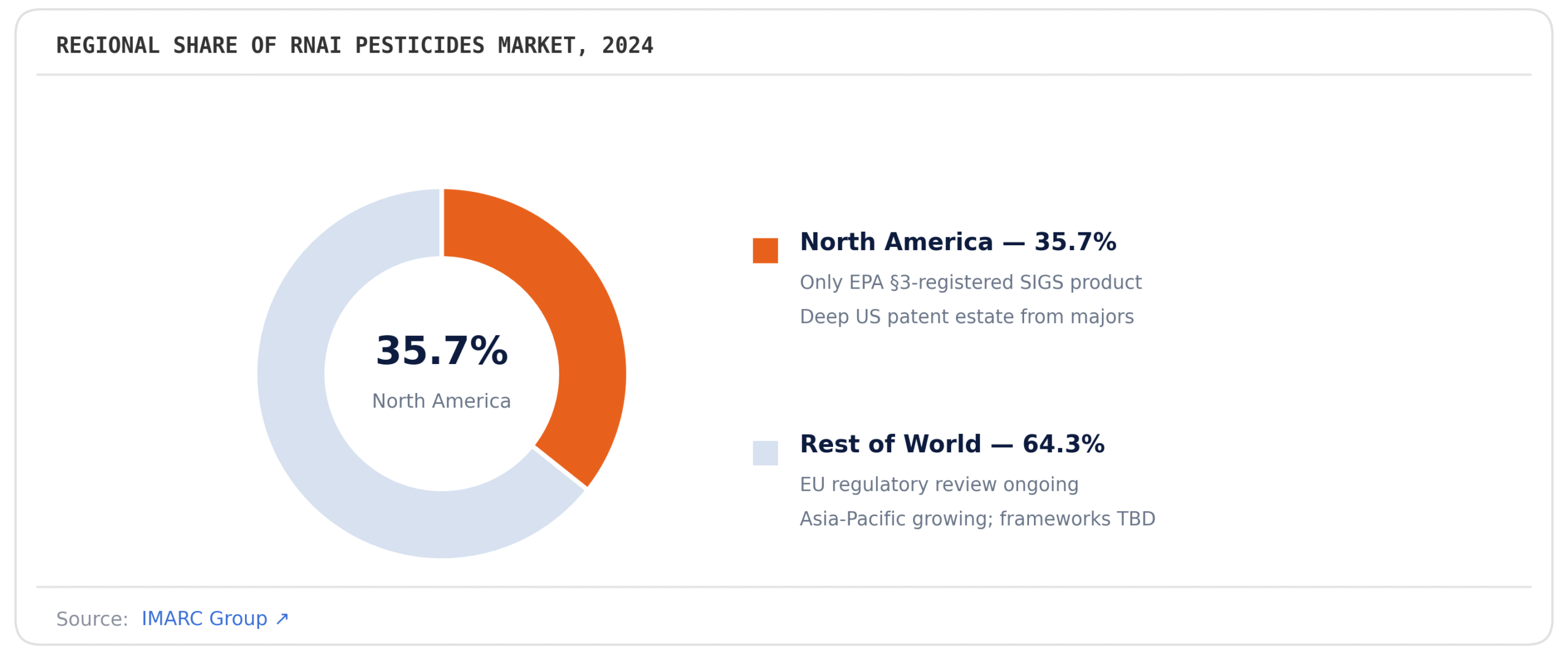

Global RNAi pesticides market is valued at $1.33 billion in 2024, reaching $3.88 billion by 2033, an 11.4% CAGR. North America, today holds the dominant 35.7% regional share of the market.

The regional skew is itself an IP signal: North America’s lead is built on a single regulatory approval (Ledprona/Calantha) plus the deep patent estates of US-headquartered majors. Europe is the wildcard, the EU is actively reviewing whether its existing pesticide regulations adequately capture RNAi products at all, and a bespoke regulatory framework could either accelerate adoption (if it creates a clear, cheaper pathway like FIFRA’s biopesticide track) or slow it (if it imposes additional dossier requirements specific to nucleic-acid actives). Companies filing now in Europe, GreenLight’s Spanish subsidiary, backed by a €35 million European Investment Bank venture-debt facility tied to the EU’s “NextGenBioPest” research collaboration with INRAE, is one example, are effectively helping shape that future framework.

Milestone timeline, 2012–2026

The sequence below traces how the category moved from acquisition-driven consolidation to a registered product to a multi-major commercialization race in roughly a decade.

2012

Syngenta acquires Devgen for $523 million, an early signal that a major agrochemical player viewed RNAi-derived gene-silencing IP as core, not peripheral, technology.

2021

Bayer licenses a dsRNA patent to GreenLight Biosciences covering a Varroa destructor mite control product, with market entry anticipated for 2024m an early example of a major out-licensing rather than internalizing a SIGS application.

May 2023

EPA approves field tests of Ledprona across 10 US states (Idaho, Maine, Michigan, Minnesota, New York, North Dakota, Oregon, Virginia, Wisconsin, Washington).

Dec 2023

EPA registers Ledprona / Calantha™, the first foliar-applied, FIFRA Section 3-registered RNA biopesticide, targeting the Colorado potato beetle, with a standard three-year re-evaluation term.

2024

Multiple parallel moves: Bayer and Evonik announce a strategic partnership (June 2024) to advance dsRNA delivery technologies; FMC partners with AgroSpheres (September 2024) on dsRNA-based actives, GreenLight expands into Brazil and secures €35M from the EIB for its European pipeline, two new RNAi active ingredients (Galquin, Vadescana) receive ISO common names.

Jan 2025

Corteva launches its first RNAi-based biopesticide commercially in select markets, the first major-agchem-branded SIGS product to reach growers.

Mar 2025

Syngenta partners with the Donald Danforth Plant Science Center to accelerate discovery of RNAi biopesticide candidates; separately, GreenLight Biosciences undergoes another ownership change after its 2023 go-private acquisition by a Fall Line Capital-led consortium.

Mar 2026

BASF acquires AgBiTech, extending its biologicals platform beyond nematicides into virus-based insect control part of a broader pattern of multinationals acquiring specialist biological-control IP rather than building it from scratch.

Player profiles: strategy in brief

Bayer

Holds the deepest legacy position via Monsanto’s corn rootworm RNAi traits (VT4PRO, with large-scale field testing through 2022–23 and a targeted 2024 commercial entry pending state registrations). On the spray side, it chose to license out a Varroa-mite dsRNA patent to GreenLight in 2021, and in 2024 partnered with Evonik specifically on delivery technology, a sign Bayer sees formulation, not target discovery, as its current gap.

Syngenta

Built an early RNAi base through the 2012 Devgen acquisition. According to industry analysis, its TYMIRIUM patent family covers dsRNA delivery methods specifically, a position described as requiring competitors to either license the technology or pursue alternative delivery routes, raising the barrier to entry for smaller players. Its 2025 collaboration with the Danforth Plant Science Center is aimed squarely at filling the discovery pipeline behind that delivery moat.

Continued investment in syngenta RNAi initiatives highlights the company’s long-term commitment to gene-silencing technologies, spanning target discovery, delivery systems, and intellectual property development for next-generation crop protection.

Corteva

Brings the largest overall patent estate in the sector roughly 5,900 granted US patents and 10,200 active patents outside the US. That scale converted into the first major-branded commercial SIGS product launch in January 2025, ahead of both Bayer and Syngenta’s spray-based offerings.

BASF & FMC

Both are pursuing a “buy the IP, bundle the portfolio” strategy: FMC’s September 2024 partnership with AgroSpheres and BASF’s March 2026 acquisition of AgBiTech (extending into virus-based insect control) show multinationals filling RNAi gaps via M&A and licensing rather than ground-up R&D.

GreenLight Biosciences

Founded 2008; raised roughly $46 million through a 2015-era Series D before going public via SPAC. Despite holding the foundational IP behind the only EPA Section 3-registered SIGS product (Ledprona), the company came within a step of bankruptcy in 2023, was taken private in an all-cash deal valuing it at roughly $45.5 million, and changed ownership again in March 2025, a cautionary tale that strong composition-of-matter and regulatory IP does not, by itself, guarantee a sustainable balance sheet in a capital-intensive category.

Signals to watch

- Delivery IP is where the action is – Watch patents on nanocarriers, lipid vesicles, polymer conjugates, and clay-based delivery systems; they’re the earliest indicators of emerging competitive white space.

- Increasingly, researchers are emphasizing the role of polymers in enabling RNAi based technology for sustainable pest management, as advanced polymer formulations can improve dsRNA stability, delivery efficiency, and persistence under field conditions.

- Regulation is diverging by region – The U.S. has established a pathway with Ledprona, while early European filings are helping shape the continent’s future RNAi regulatory framework.

- Multi-target RNAi is the next frontier – Expect growing patent activity around stacked-target constructs designed to improve durability and slow resistance development.

- M&A remains a key commercialization route – Large agrochemical players continue to acquire or license RNAi innovators rather than build capabilities in-house.

- Manufacturing economics will matter most – Cost-reducing dsRNA production technologies may become the decisive competitive advantage as RNAi products scale.

Sources

- IMARC Group

- InsightAce Analytic

- Mordor Intelligence

- Chemical & Engineering News (C&EN / ACS)

- AgroPages — Ledprona registration and field-test news

- AgroPages — GreenLight Biosciences news archive, including ISO common-name approvals (Galquin, Vadescana)

- GlobeNewswire

- BIS Research

- MDPI Agriculture

- PMC / Plant Biotechnology Journal — Qiao, Niño-Sánchez, Hamby et al., “Artificial nanovesicles for dsRNA delivery in spray-induced gene silencing for crop protection,” 2023

- PMC — “Recent Progress on Nanocarriers for Topical-Mediated RNAi Strategies for Crop Protection — A Review”

- PMC — “Application progress of plant-mediated RNAi in pest control”

- AgFunderNews

- PitchBook

- The Florida Senate — SB 196 (2025) bill text and history