While the world’s attention has been fixed on large language models and generative AI chatbots for the past three years, a quieter but arguably more consequential race has been underway: the fight to own the intellectual property behind Physical AI, the convergence of foundation models, robotics hardware, and real-world perception that will determine which companies can make machines that think, see, and act in the physical world.

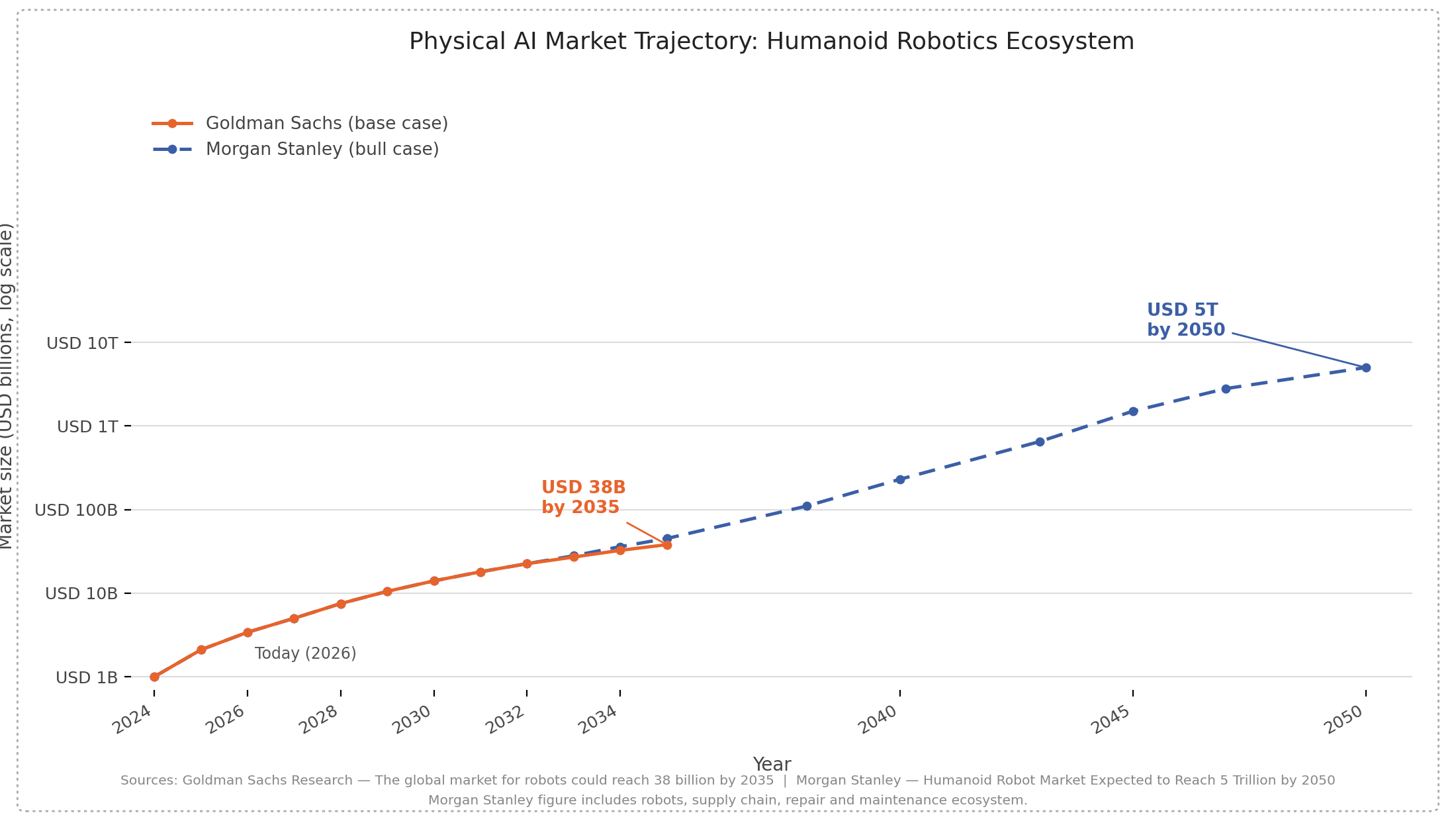

The numbers are arresting. AI-robotics publication counts, patent filings, and investment activity have all surged in recent years. Patent data confirms the acceleration: humanoid robotics patent families hit 2,592 in 2025, more than double the 1,087 filings recorded in 2023. The market behind these filings is no longer speculative. Goldman Sachs has revised its 2035 humanoid robotics market forecast upward by 6x from $6 billion to $38 billion. Morgan Stanley goes further, projecting $5 trillion by 2050 across the entire humanoid ecosystem, including robots, supply chains, and service networks.

But here is the part that most IP watchers are missing: the most valuable patents in this race have not been filed yet. The hardware layer actuators, joints, chassis is well-trafficked and increasingly commoditised. The territory where durable, defensible intellectual property will be built is the software stack sitting above the metal: Vision-Language-Action models, world models, tactile intelligence, and the operating systems that govern how robots learn and generalise. That is the frontier, and it is still remarkably open.

Volume Is Not Victory: The US–China Patent Divide

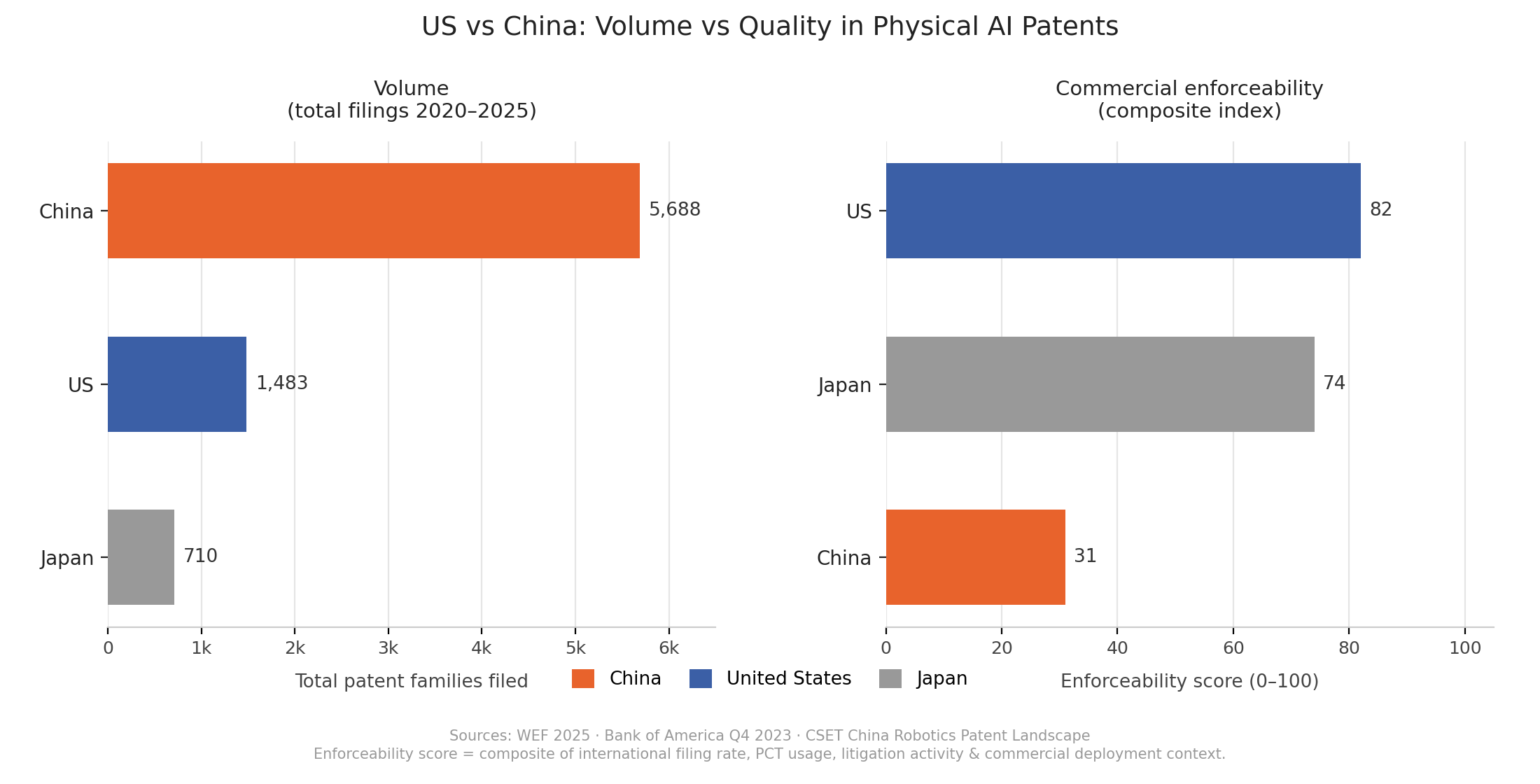

China filed 5,688 humanoid robotics patents between 2020 and 2025, against just 1,483 from the United States almost four times as many. At first glance, this looks like a decisive Chinese lead. But the picture is more complicated. Analysis of robotics-related patent filings in the technology sector found that the US held the largest share at 34% in Q4 2023, followed by China at 24% and Japan at 5%. And questions are being raised about the quality and commercial enforceability of Chinese robotics patents: during the peak of China’s filing surge, 92% of robotics patent applicants were university affiliates, and the vast majority of those patents were never filed for international use.

The pattern echoes what happened in clean energy: volume without strategic depth. China is winning the filing count. The US is building the foundation models. Google DeepMind’s RT-2 achieved a 62% success rate on novel physical scenarios versus 32% for prior approaches, by training on internet-scale data. Figure AI’s Helix foundation model, the first generalist Vision-Language-Action (VLA) model built specifically for humanoid robots runs entirely on embedded NVIDIA GPUs and generates real-time motor commands from multimodal inputs. Skild AI raised $500 million in a 2025 follow-on round to build generalised robot intelligence. Physical Intelligence raised $400 million in 2024 for the same thesis.

The divergence is strategic and intentional. American firms are prioritising core AI models and long-term platform relevance. Chinese firms are competing on manufacturing cost and filing breadth. By 2026, Unitree’s R1 humanoid was available for $5,900, a fraction of Western equivalents. But a cheap robot without proprietary intelligence is just another commodity actuator. The IP that compounds is in the model, not the metal.

The Five Battlegrounds: Where the Real IP Fight Is Happening

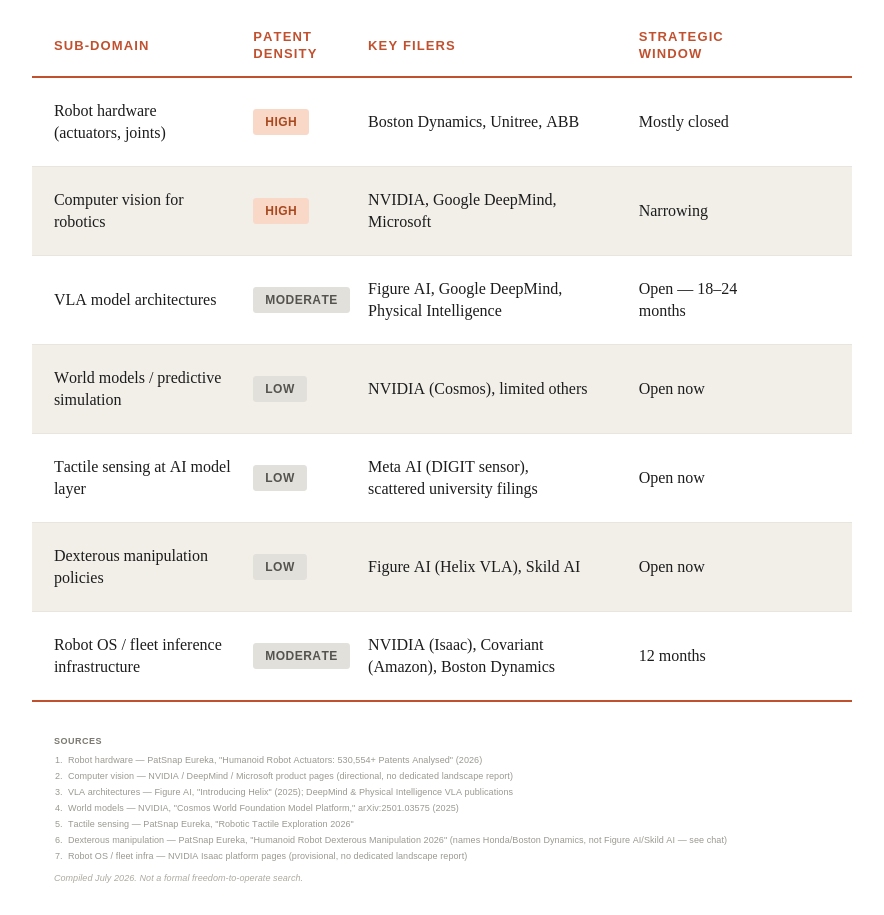

The Physical AI patent landscape is not a single front, it is five distinct technical territories, each at a different stage of competitive density. Understanding the maturity and crowding of each layer is the core of any viable patent strategy in this space.

Battleground 01

Vision-Language-Action (VLA) Models

The cognitive core of Physical AI. VLA models connect visual perception, language understanding, and motor control in unified architectures. Filing activity is accelerating but claim scope remains inconsistent, an early mover who defines the architectural primitives here can build blocking positions that persist for a decade.

Battleground 02

World Models & Predictive Control

Robots need internal representations of how the physical world behaves before they act in it. World models which simulate physics, object permanence, and causal relationships are emerging as a critical differentiator. Patent density here is strikingly low relative to the research activity, signalling a significant white space.

Battleground 03

Tactile Intelligence

Vision and language are crowded. Touch is not. Force control accuracy below 1% of rated torque and whole-body control latency under 1ms are now recognised commercial targets yet systemic patent protection for tactile sensing at the AI model layer is nascent. The filing window is narrow and closing.

Battleground 04

Dexterous Manipulation

Figure’s platform features 19 degrees of freedom per hand enabling fine manipulation that was impossible for industrial robots. But the IP protecting that manipulation capability lives in the control algorithms and learned policies, not the mechanical design. Dexterous manipulation policy patents are underrepresented relative to hardware filings.

Battleground 05

Robot Operating Systems & Inference Pipelines

NVIDIA’s Isaac and Cosmos platforms have enrolled over 500 developers. The operating infrastructure how models are deployed, updated, and personalised at the fleet level creates a platform lock-in effect equivalent to what Android created in mobile. The IP securing this layer has outsized strategic leverage.

The Thicket Risk

Increased patent filings are already generating overlapping claims and the early signs of patent thickets, dense, conflicting patent clusters that slow innovation and create litigation risk. Freedom-to-operate analysis is no longer optional; it is a prerequisite for any commercial Physical AI deployment strategy.

Competitive Filing Landscape: Who Is Protecting What

The competitive picture at the company level reveals a striking asymmetry between capital raised and IP depth built. Figure AI valued at approximately $39 billion in its most recent funding round has developed a portfolio that spans embedded actuation control, AI-based perception, joint-level cognition, and edge-based processing. That is genuine coverage across both hardware and software layers. But it is the exception rather than the rule.

The pattern here is consistent with every prior technology transition: the hardware layer fills with patents first, because hardware is legible and measurable. The software layer which ultimately captures the greater economic value gets protected later, often too late for companies that were not watching the frontier carefully. In semiconductors, the foundational architecture patents mattered far more than the fabrication equipment patents. In smartphones, operating system IP proved more valuable than handset design IP. Physical AI will follow the same curve.

The 18-Month Warning

There is a structural reason why the window matters so acutely right now. Patent applications typically take 12 to 18 months to publish after filing, meaning that a large portion of 2025 and 2026 activity is still invisible in public databases. The underlying race is faster and more crowded than the published data suggests.

This creates a specific, time-bounded strategic imperative. Companies building Physical AI capabilities today whether in VLA architectures, tactile perception pipelines, sim-to-real transfer methods, or robot operating system infrastructure have a narrow window to file foundational patents before the landscape consolidates and freedom-to-operate becomes contested territory. The transition from experimentation to commercial deployment that is now underway will accelerate that consolidation sharply.

Gartner identifies Physical AI as a top technology trend for 2026. Amazon, which reports operating one million robots today, describes Physical AI as being “about to change everything for robotics.” NVIDIA has onboarded over 500 developers onto its Cosmos and Isaac platforms. Boston Dynamics unveiled its production-ready electric Atlas at CES 2026 and immediately began commercial deployment at Hyundai factories. The race is not coming, it is here.

What Organisations Need to Do Right Now

For any organisation with a stake in Physical AI, whether as a developer, a deployer, or an investor, the strategic actions are clear and time-sensitive. First, conduct a sub-domain specific patent landscape analysis across all five battleground layers identified above, not just the hardware layer where most IP audits focus. Second, identify the architectural primitives in your own technical stack, the training methods, control architectures, inference pipelines, and sensor fusion approaches that are genuinely novel and currently unprotected. Third, commission freedom-to-operate analysis before any commercial deployment: the patent thicket risk is real and growing, and operating without FTO clearance in this space in 2026 is a material business risk, not just a legal one.

The companies that will own Physical AI are not necessarily the ones with the most impressive robots in 2026. They are the ones that correctly identify which layer of the stack captures lasting value and file the right patents, in the right jurisdictions, before the window closes.

The body of the robot is a commodity. The mind of the robot is the patent.