The global agrochemicals market is currently valued at approximately $299.7 billion and is projected to reach $449.9 billion by 2033.# While this growth is significant, the more important story lies in how the industry itself is evolving.

Agriculture is undergoing a fundamental transformation. Traditional synthetic chemistry, which has long dominated crop protection and productivity strategies, is increasingly being complemented by biological products, AI-assisted discovery platforms, gene-edited crops, and precision agriculture technologies.

The Rise of Biologicals

The growth of biological products remains one of the most significant developments in the agrochemical sector.

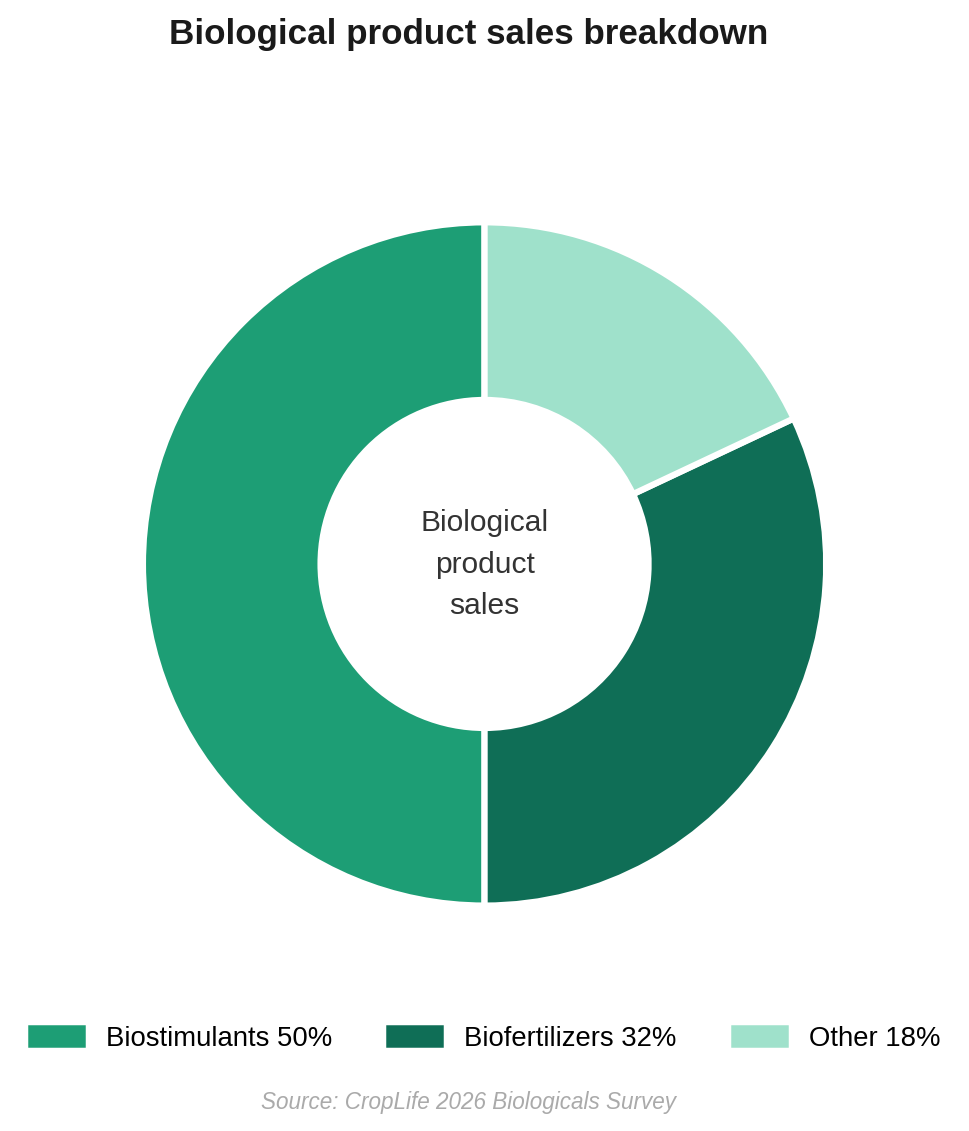

By the end of 2025, the global biologicals market had reached approximately $17 billion, while biological products generated more than $3.5 billion in revenue in the United States alone. The figure below depicts the market share distribution of biologics used in agriculture.

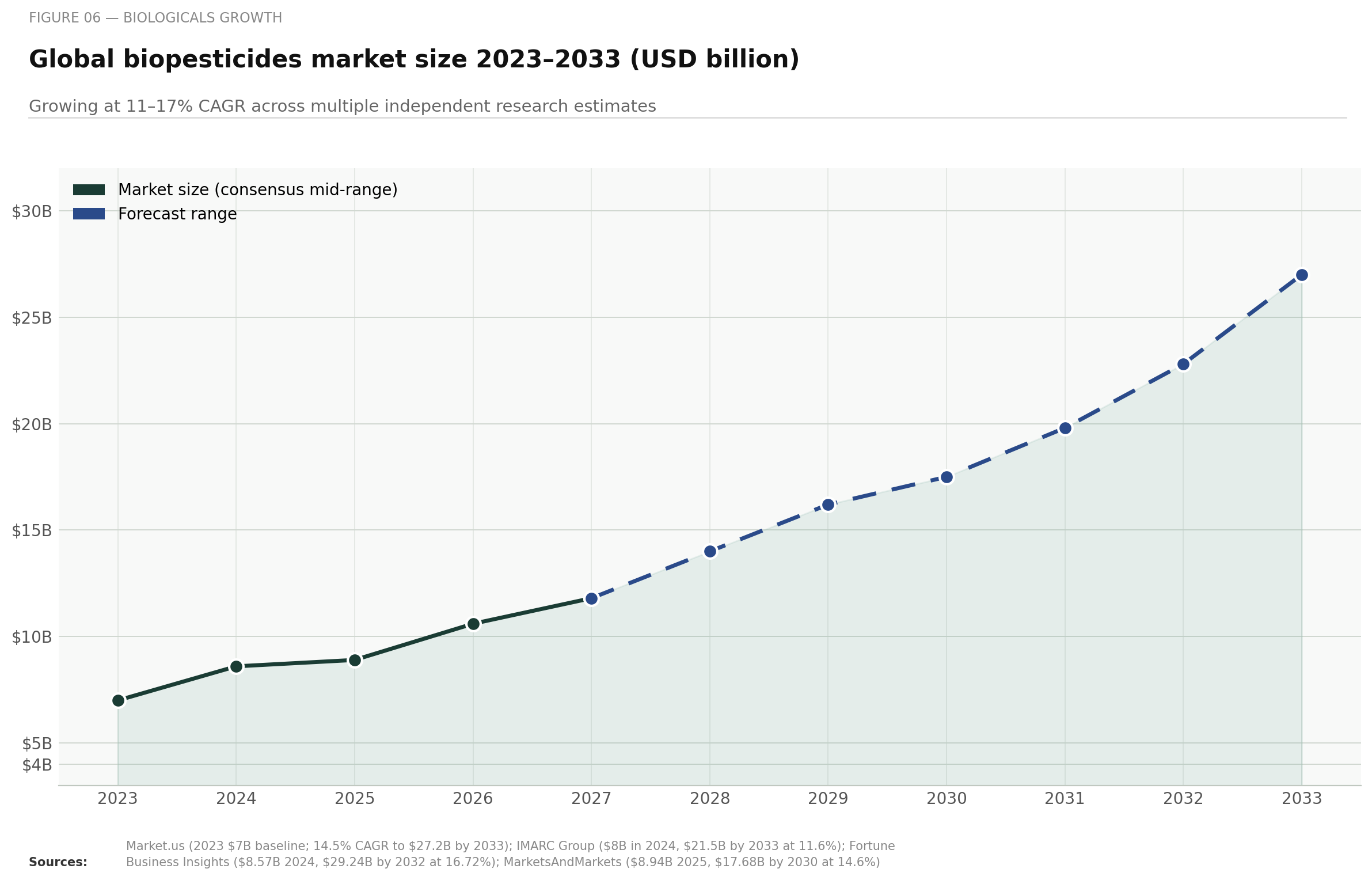

Within bio stimulants, the projected growth of the global biopesticides market reflects a broader structural shift taking place across agriculture.

According to industry estimates, the global biopesticides market is expected to grow from approximately USD 8.3 billion in 2025 to more than USD 26 billion by 2033, representing a compound annual growth rate (CAGR) of over 15%. This makes biopesticides one of the fastest-growing segments within the broader crop protection industry.

Much of this expansion is being driven by microbial-based products, which account for more than 50% of the global biopesticides market. These products are increasingly being adopted because of their targeted modes of action, lower environmental persistence, and compatibility with integrated pest management (IPM) systems.

Regional growth patterns also highlight the changing geography of agricultural innovation. Asia-Pacific currently accounts for more than 36% of global biopesticides revenue and is expected to remain the fastest-growing market through 2033, supported by expanding agricultural production, government support for sustainable farming, and increasing pressure to reduce chemical pesticide dependence.

The rapid growth of biological crop protection products is also influencing intellectual property strategies across the sector. Companies are increasingly seeking patent protection not only for microbial strains and biological active ingredients, but also for fermentation processes, formulation technologies, encapsulation systems, seed-treatment applications, and controlled-release delivery mechanisms.

AI-Led Agrochemical Innovation

Artificial intelligence is no longer limited to improving existing products. It is increasingly being used to discover entirely new crop protection molecules, helping researchers identify promising candidates long before they reach the laboratory.

Traditionally, developing a new agrochemical required screening thousands of compounds through years of testing. Today, AI can analyze vast chemical, biological, and genomic datasets to predict efficacy, toxicity, environmental impact, and resistance risks, significantly reducing discovery timelines and R&D costs.

One notable example comes from Syngenta, which invests approximately $2 billion annually in R&D and has used machine learning to support the development of a novel herbicide aimed at tackling herbicide-resistant weeds, one of agriculture’s fastest-growing challenges.

Similarly, Corteva and Hexagon Bio are combining AI, microbial genetics, and synthetic biology to discover entirely new crop protection compounds by analyzing microbial genomes and natural-product databases, rather than relying solely on traditional chemical screening.

Beyond molecule discovery, AI is increasingly being used to optimize formulations, improve product stability, predict pest outbreaks, and support resistance-management strategies.

At the same time, innovation in delivery technologies, including slow-release encapsulation systems, precision seed coatings, and variable-rate application methods, is creating new opportunities for intellectual property protection. In many cases, these technologies provide stronger competitive advantages than the active ingredient itself.

Marine-Derived Agricultural Inputs

Marine Based Researchers are also exploring marine-derived biological ingredients, opening entirely new categories of crop protection and plant health products.

A Shift from Products to Platforms

The industry’s business model is also evolving.

For farmers, the value proposition is changing. Instead of purchasing individual products, they are increasingly adopting broader crop-management systems designed to optimize productivity, sustainability, and profitability.

This shift has significant implications for intellectual property strategy. Agronomic algorithms, predictive analytics platforms, farm intelligence systems, and decision-support software are becoming valuable proprietary assets.

Ownership of the data layer, the systems that determine how agricultural inputs are used may ultimately prove more commercially valuable than ownership of any single crop protection product.

Precision Agriculture and the New Value Chain

Precision agriculture technologies continue to expand across global farming systems.

Advanced application technologies allow farmers to reduce chemical use while maintaining productivity. At the same time, digital platforms provide real-time insights that improve decision-making and resource allocation.

Another important development is the growing integration of genetics and crop protection technologies.

The European Commission’s recent progress on the regulatory framework for New Genomic Techniques (NGTs) reflects increasing recognition of the role that gene-edited crops can play in sustainable agriculture. These technologies enable the development of crops with enhanced resilience to drought, heat stress, and disease, potentially reducing reliance on chemical inputs.

For innovators, this creates opportunities that extend beyond individual products. Intellectual property strategies can now span multiple components of the agricultural value chain, from genetic traits and biological products to application technologies and digital management systems.

The boundaries that once separated seeds, chemistry, and biologicals are becoming increasingly blurred.

Regulation Is Reshaping Innovation Priorities

While market demand remains an important driver of innovation, regulatory developments are having an equally significant impact.

For agrochemical companies, these policies have practical implications. Products that cannot demonstrate environmental sustainability may face increasing regulatory barriers and reduced market access.

As a result, investment in biological products, precision application technologies, and digital decision-support systems is increasingly becoming a strategic necessity rather than a voluntary sustainability initiative.

In many respects, regulation has emerged as one of the most powerful forces shaping agricultural innovation in 2026.

Where Patent Activity Is Concentrated

Perhaps the clearest indicator of where the agrochemical industry is heading is where companies are filing patents.

In 2026, patent activity is increasingly concentrated around five high-value innovation zones, each representing a different piece of agriculture’s future technology stack.

- Microbial Strains and Biological Formulations

Companies are aggressively protecting novel microorganisms, biological pesticides, bio stimulants, fermentation technologies, and proprietary biological formulations. As biologicals become mainstream, ownership of unique strains and production methods is becoming a major competitive advantage.

- Delivery and Encapsulation Technologies

In many cases, the delivery system is becoming as valuable as the active ingredient itself. Patent filings are rising around slow-release formulations, nano-encapsulation systems, seed coatings, drift-reduction technologies, and precision application platforms designed to improve efficacy while reducing environmental impact.

- AI-Driven Discovery Platforms

Artificial intelligence is creating an entirely new category of intellectual property. Companies are seeking protection not only for AI-discovered molecules, but also for the algorithms, computational models, screening platforms, and data systems used to identify them. As AI becomes embedded in R&D, ownership of discovery platforms may prove as valuable as ownership of the products they generate.

- Digital Agriculture and Farm Intelligence Systems

Patent filings are expanding beyond chemistry into software. Predictive analytics platforms, agronomic decision-support tools, farm intelligence systems, pest forecasting models, and precision agriculture software are emerging as critical proprietary assets in the digital farming ecosystem.

- Climate-Resilient Crop Traits

As climate volatility increases, innovation is increasingly focused on crops that can withstand drought, heat, salinity, and emerging disease pressures. Advanced breeding technologies, gene-editing platforms, and novel genetic traits continue to attract substantial patent activity as companies race to develop more resilient agricultural systems.

Conclusion

The agrochemical industry by 2033 is unlikely to resemble the sector that existed a decade ago. Biological products will play a larger role in crop protection. Artificial intelligence will increasingly influence discovery and development. Precision agriculture technologies will continue to reshape farm management practices. Regulatory expectations will place sustainability at the center of innovation strategies.

Most importantly, the industry’s most valuable intellectual property assets will no longer be limited to molecules alone. Future competitive advantages will increasingly be built across biological systems, digital platforms, delivery technologies, data infrastructure, and advanced genetics.

The evidence is already visible in market data, regulatory developments, patent filings, and strategic partnerships across the sector. The companies that recognize this transformation as a long-term platform shift, rather than a short-term product cycle, are likely to be the ones that define the future of agriculture.