India’s electric mobility story is often presented as an uninterrupted success. EV registrations continue to rise; manufacturers are expanding their portfolios, and policymakers are investing heavily in the transition. Yet beneath the optimism lies a more difficult reality: the next phase of EV growth will be determined not by adoption alone, but by whether India can solve deep structural challenges around affordability, infrastructure, battery technology, and intellectual property.

The first wave of EV adoption was driven by incentives, early adopters, and favorable economics in segments such as two-wheelers and three-wheelers. The next phase requires something far more difficult; an ecosystem capable of supporting mass-market adoption at scale.

EV Adoption Is Growing, But Unevenly

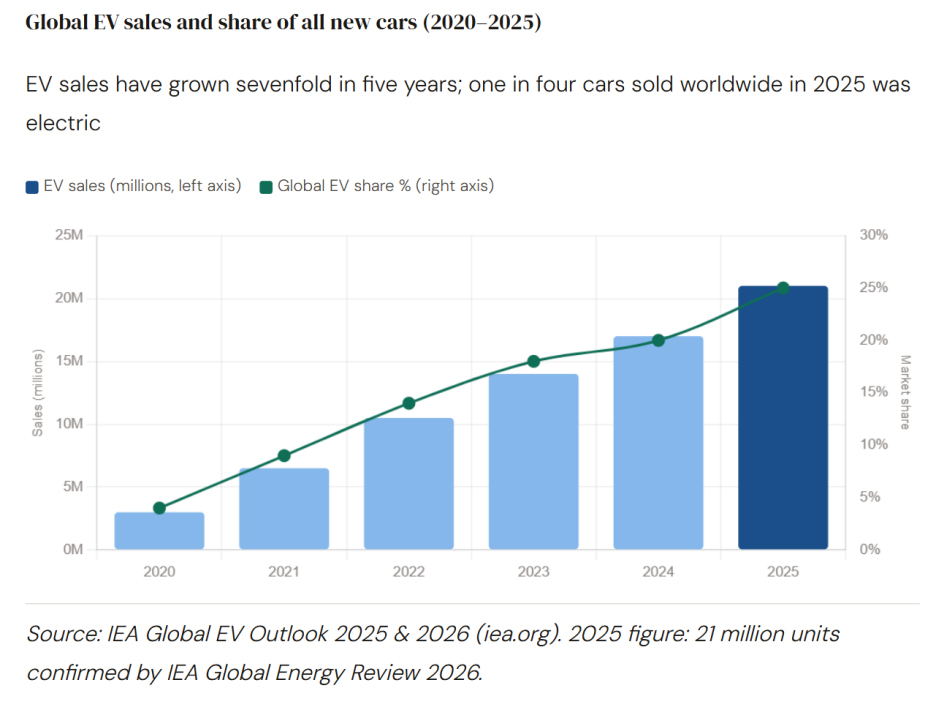

Global EV momentum remains strong. According to the International Energy Agency (IEA), global electric car sales exceeded 20 million units in 2025, accounting for approximately 25% of all new car sales worldwide.

India has participated in this growth story, particularly in smaller vehicle segments. The IEA identifies India as the world’s largest electric three-wheeler market, with electric three-wheeler sales reaching approximately 700,000 units in 2024. EV registrations in India approached 2 million units during FY2025, reflecting strong demand across commercial and urban mobility applications.

However, success has not been uniform. Adoption remains strongest in vehicle categories where operating-cost savings are immediately visible. Passenger vehicle adoption, by contrast, remains relatively limited compared to conventional alternatives.

This raises an uncomfortable question: has India solved the easy part of electrification while the harder challenges remain ahead?

Charging Infrastructure Is Expanding, But Reliability Matters More Than Quantity

India has made significant progress in public charging deployment, with more than 25,000 public charging stations installed nationwide.

Yet infrastructure challenges remain a recurring concern for EV users. Industry participants continue to highlight issues relating to maintenance, interoperability, charger availability, and network consistency across regions.

The next stage of infrastructure development is therefore not simply about installing more chargers. The next phase of EV adoption will depend on building charging networks that are both interoperable and climate resilient.

This means creating infrastructure that works seamlessly across different vehicle brands, charging operators, and payment systems, allowing drivers to charge their vehicles without compatibility concerns. At the same time, charging stations must be designed to withstand increasingly common climate-related challenges such as extreme heat, heavy rainfall, flooding, and dust exposure. Most importantly, these networks need to deliver a reliable and consistent user experience, ensuring that consumers can depend on them for their daily commuting and transportation needs.

Cost Competitiveness Depends on the Battery Ecosystem

India’s EV market has demonstrated that consumers and commercial operators are willing to adopt electric mobility, particularly in two-wheelers and three-wheelers. The more significant economic challenge lies deeper in the value chain.

Battery packs remain one of the most important cost components in electric vehicles, and India continues to rely heavily on imported battery cells and critical minerals. This dependence exposes manufacturers to global supply-chain disruptions, commodity-price volatility, and currency fluctuations, while limiting their ability to control costs through domestic production.

The contrast with China is particularly striking. According to the International Energy Agency (IEA), approximately 70% of battery-electric cars sold in China are already cheaper than the average conventional vehicle. That level of cost competitiveness was enabled by large-scale battery manufacturing, supply-chain localization, and sustained investment in battery innovation.

For India, the challenge is not merely to increase EV sales. It is to build the domestic battery ecosystem required to reduce technological dependence, improve cost competitiveness, and capture a larger share of value from the global electric mobility transition.

The Real Competition Is in Batteries and Intellectual Property

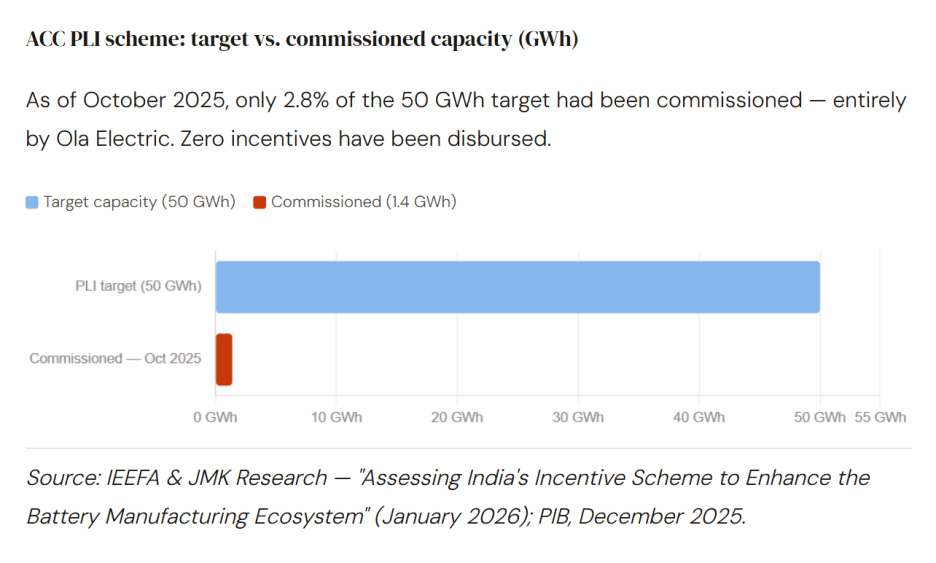

One of the most significant long-term risks facing India’s EV ecosystem is technological dependence. Recognizing this challenge, the Government of India launched the Advanced Chemistry Cell (ACC) Production Linked Incentive Scheme with an outlay of ₹18,100 crore and a target of 50 GWh of domestic battery manufacturing capacity.

However, government disclosures indicate that only around 1 GWh of manufacturing capacity had been installed by late 2025. The gap between policy ambition and manufacturing reality remains substantial.

More importantly, the future EV market is increasingly being shaped by intellectual property.

According to the IEA, battery-related technologies account for roughly half of all energy-sector patenting activities worldwide. The companies that control advanced battery chemistry, thermal management systems, battery-management software, recycling technologies, and energy-storage innovations are likely to capture a disproportionate share of future value.

For India, assembling EVs may not be enough. Long-term competitiveness will depend on building proprietary technology and strong patent portfolios across the battery value chain.

The Future of EVs Is Also a Software Race

Electric vehicles are rapidly evolving into software-defined products.

Competition increasingly revolves around smart charging, cybersecurity, connected mobility platforms, predictive analytics, energy management systems, and vehicle-to-grid integration. In several leading EV markets, software ecosystems have become as important as vehicle hardware.

This has important implications for Indian manufacturers. Success in the next decade may depend not only on manufacturing capability, but also on the ability to develop software platforms that create value beyond the vehicle itself.

The Road Ahead

India possesses several advantages that many countries lacked during their own EV transitions: a large domestic market, strong engineering talent, growing policy support, and one of the world’s most dynamic digital ecosystems.

Yet growth alone should not be mistaken for readiness.

The real test of India’s EV transition will not be how many vehicles are sold over the next few years. It will be whether the country can build reliable charging infrastructure, reduce battery dependence, develop globally competitive intellectual property, and establish leadership in the technologies that will define the future of mobility.

The opportunity is enormous. But so is the gap between where the ecosystem is today and where it ultimately needs to be.

Sources:

- https://www.iea.org/reports/global-ev-outlook-2026/trends-in-electric-cars

- https://www.iea.org/reports/global-ev-outlook-2025/executive-summary

- https://www.iea.org/reports/global-ev-outlook-2025

- https://www.pib.gov.in

- https://pib.gov.in/PressReleasePage.aspx?PRID=2224542

- https://beeindia.gov.in

- https://powermin.gov.in

- India battles power cuts as heatwave boosts electricity demand to record | Reuters